🏷️ LIMITED TIME OFFER: GET 20% OFF GRADE+ YEARLY SUBSCRIPTION →

Pricing

Log in

Sign up

Home

Homework Help

Study Guides

Class Notes

Textbook Notes

Textbook Solutions

Booster Classes

Blog

Home

Textbook Notes

300,000

CA

170,000

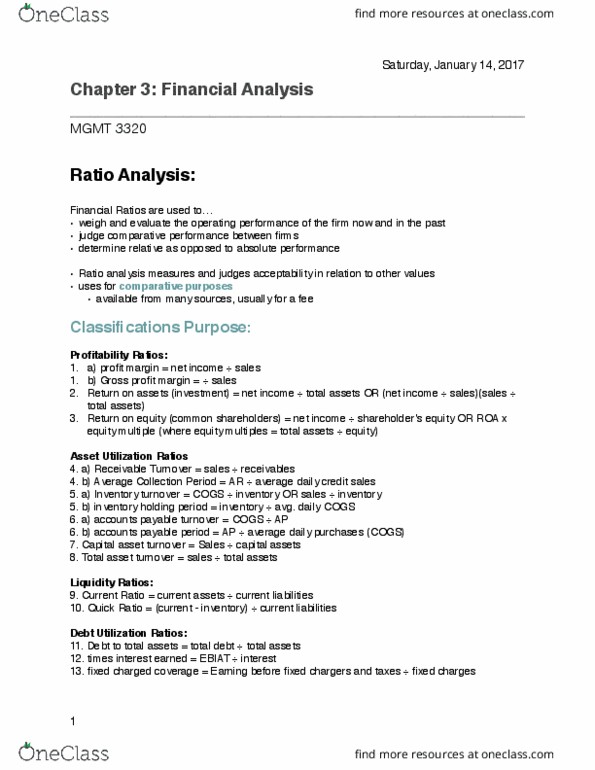

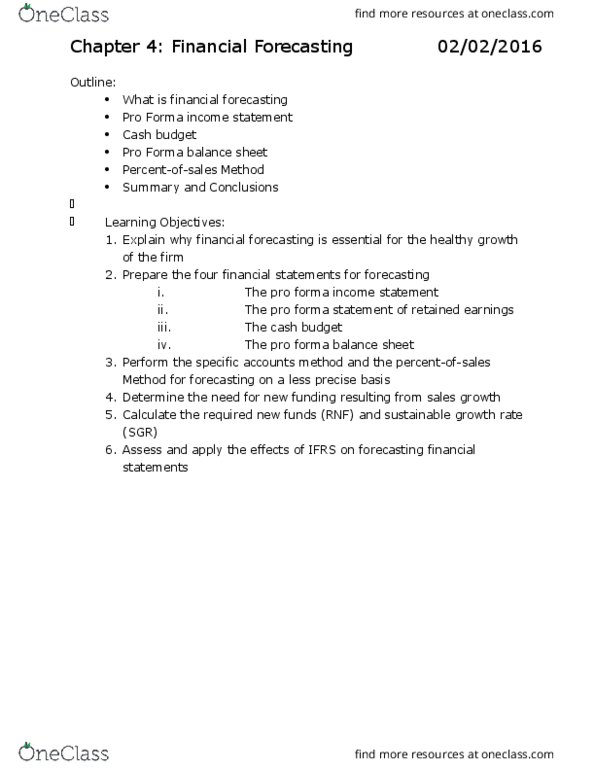

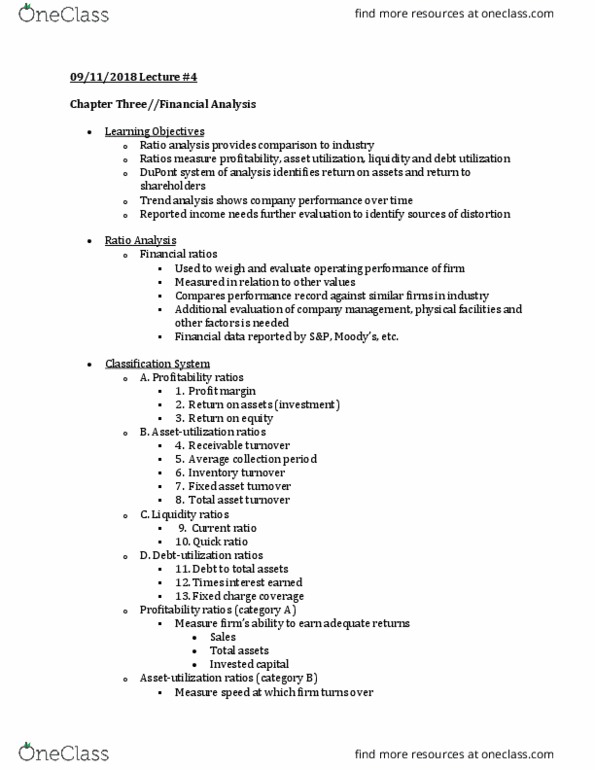

MGMT 3320 Chapter Notes - Chapter 3: Disinflation, Asset Turnover, Cash Conversion Cycle

112

views

19

pages

yellowworm378

23 Mar 2016

School

University of Guelph

Department

Management

Course

MGMT 3320

Professor

Elliot Currie

Like

For unlimited access to Textbook Notes, a

Class+

subscription is required.

Get access

Yearly

Monthly

Yearly

Grade+

20% off

$8

USD/m

$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8

USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Continue

Related Documents

MGMT 3320 Chapter Notes - Chapter 3: Asset Turnover, Root Mean Square, Accounts Payable

whitepanda307

MGMT 3320 Chapter Notes - Chapter 4: Accounts Payable, Current Liability, Promissory Note

yellowworm378

BUS 320 Lecture Notes - Lecture 4: Asset Turnover, Inventory Turnover, Quick Ratio