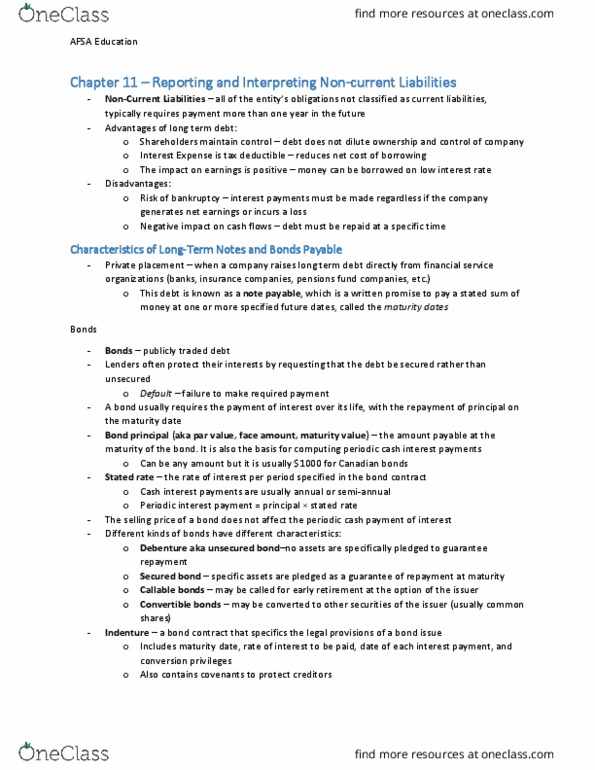

AFM101 Chapter Notes - Chapter 11: Effective Interest Rate, Interest Expense, Current Liability

Get access

Related Documents

Related Questions

1. Use the attached balance sheet and income statement to compute the required financial ratios for 2012. Use 360 for the number of days in a year. The computations for 2011 are already done for you.

Current ratio_________________________

Quick ratio__________________________

Inventor turnover____________________

Average Collection Period_____________

Total asset turnover__________________

Net profit margin____________________

Operating profit margin_______________

Times Interest Earned_________________

Debt/Net Worth Ratio_________________

Return on Equity ratio__________________

2. Using the computed financial ratios from question 1, compare Grounds Keeperâs performance from 2011 to 2012. Address what areas the company has improved and what areas it has not

A.)Liquidity

B.) Activity / turnover / efficiency

C.) Profitability

D.) Leverage / use of debt / solvency

3. If you were the CEO of Grounds Keeper, what area(s) would you concentrate on to improve the performance of the company?

4. Define the terms capital structure, cost of capital, and working capital. Focus on how they are different from each other and impact both profitability and risk.

5. Determine Grounds Keeperâs capital structure and working capital.

6. If Grounds Keeper has a required rate of return on its long-term debt of 9% (before taxes) and a required rate of return on its common stock, a tax rate of 40%, what is its weighted average cost of capital (WACC) for 2012? How could Grounds Keeper lower its WACC? (HINT: you will need to look at the balance sheet to determine the weight of debt to equity.

7. What are the advantages to Grounds Keeper in using money market instruments as financing? How does this related to financing net working capital?

8. Explain what Grounds Keeper should consider when deciding whether to issue stocks or bonds? Answer using at least 3 different characteristics comparing and contrasting stocks and bonds.

9. Define money market instruments; list at least one type of security that would be considered a money market instrument. What are the advantages to Grounds Keeper in using money market instruments as financing? What are the disadvantages?

| Grounds Keeper | ||

| Consolidated Balance Sheets | ||

| (Dollars in thousands) | ||

| 2012 | 2011 | |

| Assets | ||

| Current assets: | ||

| Cash and cash equivalents | 78,240 | 44,395 |

| Receivables | 399,891 | 340,062 |

| Inventories | 844,737 | 736,677 |

| Total current assets | 1,322,868 | 1,121,133 |

| Fixed assets, net | 1,244,384 | 889,613 |

| Other long-term assets | 1,048,537 | 1,187,141 |

| Total assets | 3,615,789 | 3,197,887 |

| Liabilities and Stockholdersâ Equity | ||

| Current liabilities: | ||

| Accounts payable | 309,222 | 319,465 |

| Accruals | 201,017 | 145,240 |

| Notes payable | 9,748 | 6,669 |

| Total current liabilities | 519987 | 471374 |

| Long-term debt | 834574 | 814298 |

| Total liabilities | 1,354,561 | 1,285,672 |

| Stockholdersâ equity: | ||

| Common stock, $0.10 par value: | 15,268 | 15,447 |

| Additional paid-in capital | 1,464,560 | 1,499,616 |

| Retained earnings | 781400 | 397152 |

| Total stockholdersâ equity | 2,261,228 | 1,912,215 |

| Total liabilities and stockholdersâ equity | 3,615,789 | 3,197,887 |

| Grounds Keeper | |||||

| Consolidated Statements of Operations | |||||

| (Dollars in thousands except per share data) | |||||

| 2011 | ||||

| Net sales | 3,889,426 | 2,642,390 | |||

| Cost of sales | 2,589,799 | 1,746,274 | |||

| Gross profit | 1,299,627 | 896,116 | |||

| Selling and operating expenses | 481,493 | 348,696 | |||

| General and administrative expenses | 219,010 | 187,016 | |||

| Operating income | 599,124 | 360,404 | |||

| Interest expense | 22,983 | 57,657 | |||

| Income before income taxes | 576,141 | 302,747 | |||

| Income tax expense | 212,641 | 101,699 | |||

| Net Income | 363,500 | 201,048 | |||

| Basic income per share: | |||||

| Average shares outstanding | 154,933,948 | 146,214,860 | |||

| Earnings per common share | 2.35 | 1.38 |

| Current Ratio | Current assets/ Current liabilities |

| Quick Ratio | Current assets â inventory/ Current liabilities |

| Inventory Turnover | Cost of goods sold/ Inventory |

| Receivables Turnover | Sales/ Accounts receivables |

| Average Collection Period | Receivables/ Sales per day |

| Fixed Asset Turnover | Sales/ Fixed assets |

| Total Asset Turnover | Sales/ Total Assets |

| Gross Profit Margin | Revenues - Cost of goods sold/ Sales |

| Operating Profit Margin | Earnings before interest and taxes/ Sales |

| Net Profit Margin | Net income/ Sales |

| Return on Total Assets | Net income/ Total assets |

| Debt/Net Worth Ratio | Total Debt/ Total Equity |

| Times-Interest-Earned | Operating Income/ Interest expense |

| Return on Equity | Net income/ Total equity |

Compare Companies --- Netflix (NFLX) vs. GEO Holdings (TOK) Compute financial ratios, time value, variables, and returns using industry standard tools for optimizing financial success. Analyze corporate financial data in evaluating past and future financial performances.

Use formulas to calculate the following financial indicators for each year of data: Three fiscal years for Netflix and GEO Holdings for:

o Price to earnings ratio

o Debt to equity ratio

o Free cash flow

o Earnings per share

o Return on equity

o Net profit margin

V. Performance Over Time

A. Analyze the performance of the Netflix over time. What financial strengths and weaknesses does this company have? Consider addressing the free cash flows and ratios you calculated earlier.

B. Analyze the performance of your GEO Holdings over time. What financial strengths and weaknesses does this company have? Consider addressing the free cash flows and ratios you calculated earlier.

C. Analyze how the data differ between these two companies. Why do you think this is? Consider addressing the free cash flows and ratios you calculated earlier.

VI. Investment

A. Are the companies considered growth or value companies? Why?

B. Which companyâs stock is the better investment?

| Netflix Inc. (NMS: NFLX) | |||||

| Exchange rate used is that of the Year End reported date | |||||

| As Reported Annual Balance Sheet | |||||

| Report Date | 12/31/2016 | 12/31/2015 | 12/31/2014 | ||

| Currency | USD | USD | USD | ||

| Audit Status | Not Qualified | Not Qualified | Not Qualified | ||

| Consolidated | Yes | Yes | Yes | ||

| Scale | Thousands | Thousands | Thousands | ||

| Cash & cash equivalents | 1467576 | 1809330 | 1113608 | ||

| Short-term investments | 266206 | 501385 | 494888 | ||

| Current content library, net | - | - | 2125702 | ||

| Current content assets, net | 3726307 | 2905998 | - | ||

| Other current assets | 260202 | 215127 | 206271 | ||

| Total current assets | 5720291 | 5431840 | 3940469 | ||

| Non-current content library, net | - | - | 2773326 | ||

| Non-current content assets, net | 7274501 | 4312817 | - | ||

| Information technology assets | 185345 | 194054 | 189274 | ||

| Furniture & fixtures | 32185 | 30914 | 25758 | ||

| Building | 40681 | 40681 | 40681 | ||

| Leasehold improvements | 107945 | 107793 | 57339 | ||

| DVD operations equipment | 70152 | 88471 | 89144 | ||

| Capital work-in-progress | 108296 | 8845 | 12495 | ||

| Property & equipment, gross | 544604 | 470758 | 414691 | ||

| Less: accumulated depreciation | 294209 | 297346 | 264816 | ||

| Property & equipment, net | 250395 | 173412 | 149875 | ||

| Other non-current assets | 341423 | 284802 | 192981 | ||

| Total assets | 13586610 | 10202871 | 7056651 | ||

| Current content liabilities | 3632711 | 2789023 | 2117241 | ||

| Accounts payable | 312842 | 253491 | 201581 | ||

| Accrued expenses | 197632 | 140389 | 69746 | ||

| Deferred revenue | 443472 | 346721 | 274586 | ||

| Total current liabilities | 4586657 | 3529624 | 2663154 | ||

| Non-current content liabilities | 2894654 | 2026360 | 1575832 | ||

| Long-term debt | 3364311 | 2371362 | 900000 | ||

| Other non-current liabilities | 61188 | 52099 | 59957 | ||

| Total liabilities | 10906810 | 7979445 | 5198943 | ||

| Common stock | 1599762 | 1324809 | 60 | ||

| Additional paid-in capital | - | - | 1042810 | ||

| Foreign currency | -47966 | -42502 | -4615 | ||

| Change in unrealized gains on available for sale securities | -599 | -806 | 169 | ||

| Accumulated other comprehensive income (loss) | -48565 | -43308 | -4446 | ||

| Retained earnings (accumulated deficit) | 1128603 | 941925 | 819284 | ||

| Total stockholders' equity (deficiency) | 2679800 | 2223426 | 1857708 |

| Geo Holdings Corp (TOK: 2681) | |||||

| Due to changes with International Financial Reporting Standards (IFRS), recent financials statement presentations have been adjusted to meet this standard. Please note the original historical presentations have remained in the original format | |||||

| Exchange rate used is that of the Year End reported date | |||||

| As Reported Annual Balance Sheet | |||||

| Report Date | 03/31/2016 | 03/31/2015 | 03/31/2014 | ||

| Currency | JPY | JPY | JPY | ||

| Audit Status | Not Qualified | Not Qualified | Not Qualified | ||

| Consolidated | Yes | Yes | Yes | ||

| Scale | Millions | Millions | Thousands | ||

| Cash & deposits | 37683 | 32052 | 19869000 | ||

| Trade notes & accounts receivables | 4100 | 4077 | 3992000 | ||

| Merchandise | 24894 | 23834 | 23495000 | ||

| Deferred tax assets | 2156 | 1806 | 1773000 | ||

| Other current assets | 5462 | 7181 | 5942000 | ||

| Allowance for doubtful accounts | -281 | -292 | 343000 | ||

| Total current assets | 74015 | 68659 | 54729000 | ||

| Asset for rent, gross | 100974 | 104514 | 104647000 | ||

| Accumulated depreciation - asset for rent | -95154 | -97475 | 96055000 | ||

| Asset for rent, net | 5820 | 7038 | 8591000 | ||

| Buildings & structures, gross | 40872 | 39984 | 39478000 | ||

| Accumulated depreciation - buildings & structures | -27470 | -26362 | 25976000 | ||

| Buildings & structures, net | 13402 | 13622 | 13501000 | ||

| Land, net | 5844 | 6356 | 6651000 | ||

| Leased assets, gross | 2176 | 3519 | 4576000 | ||

| Accumulated depreciation - leased assets | -681 | -1764 | 2588000 | ||

| Leased assets, net | 1495 | 1754 | 1988000 | ||

| Other property, plant & equipment, gross | 24838 | 20562 | 17708000 | ||

| Accumulated depreciation - other property, plant & equipment | -18391 | -15292 | 13236000 | ||

| Other property, plant & equipment, net | 6447 | 5270 | 4471000 | ||

| Total property, plant & equipment | 33010 | 34043 | 35205000 | ||

| Total intangible assets | 1865 | 1277 | 2028000 | ||

| Investment securities | 926 | 1002 | 1266000 | ||

| Long-term loans receivable | 2250 | 6682 | 6628000 | ||

| Lease & guarantee deposits | 14905 | 14735 | 15034000 | ||

| Deferred tax assets | 3342 | 3774 | 2845000 | ||

| Other investments & other assets | 1222 | 1188 | 1760000 | ||

| Allowance for doubtful accounts | -1332 | -3751 | 3917000 | ||

| Total investments & other assets | 21315 | 23632 | 23617000 | ||

| Total non-current assets | 56192 | 58952 | 60851000 | ||

| Total assets | 130207 | 127612 | 115581000 | ||

| Trade accounts payable | 12631 | 13540 | 13124000 | ||

| Current portion of long-term borrowings | 8333 | 7097 | 8754000 | ||

| Current portion of bonds | 149 | 149 | 249000 | ||

| Income taxes payable | 4815 | 265 | 1170000 | ||

| Reserve for bonuses | 1665 | 1420 | 1135000 | ||

| Other current liabilities | 10135 | 12595 | 10279000 | ||

| Total current liabilities | 37731 | 35068 | 34713000 | ||

| Bonds | 105 | 254 | 403000 | ||

| Long-term borrowings | 19509 | 21843 | 13910000 | ||

| Lease liabilities | 1612 | 1660 | 1590000 | ||

| Deferred tax liabilities | 23 | 22 | 26000 | ||

| Asset retirement obligations | 4406 | 3994 | 3898000 | ||

| Other non-current liabilities | 1857 | 1554 | 1839000 | ||

| Total non-current liabilities | 27514 | 29329 | 21668000 | ||

| Total liabilities | 65246 | 64398 | 56381000 | ||

| Capital stock | 8871 | 8615 | 8603000 | ||

| Capital surplus | 3283 | 6090 | 6078000 | ||

| Retained earnings | 52542 | 49998 | 44381000 | ||

| Treasury shares | - | -1979 | 334000 | ||

| Total shareholders' equity | 64697 | 62724 | 58729000 | ||

| Valuation difference on available-for-sale securities | 166 | 282 | 297000 | ||

| Loss (gain) on deferred hedge | -15 | - | 297000 | ||

| Total accumulated other comprehensive income | 150 | 282 | 172000 | ||

| Stock acquisition rights | 113 | 206 | 59199000 | ||

| Net assets | 64961 | 63214 | 115581000 | ||

| Total liabilities & net assets | 130207 | 127612 |

| Netflix Inc. (NMS: NFLX) | |||||

| Exchange rate used is that of the Year End reported date | |||||

| As Reported Annual Income Statement | |||||

| Report Date | 12/31/2016 | 12/31/2015 | 12/31/2014 | ||

| Currency | USD | USD | USD | ||

| Audit Status | Not Qualified | Not Qualified | Not Qualified | ||

| Consolidated | Yes | Yes | Yes | ||

| Scale | Thousands | Thousands | Thousands | ||

| Revenues | 8830669 | 6779511 | 5504656 | ||

| Cost of revenues | 6029901 | 4591476 | 3752760 | ||

| Marketing expenses | 991078 | 824092 | 607186 | ||

| Technology & development expenses | 852098 | 650788 | 472321 | ||

| General & administrative expenses | 577799 | 407329 | 269741 | ||

| Operating income (loss) | 379793 | 305826 | 402648 | ||

| Interest expense | 150114 | 132716 | 50219 | ||

| Interest & other income (expense) | 30828 | -31225 | -3060 | ||

| Income before income taxes - United States | 188078 | 95644 | 325081 | ||

| Income (loss) before income taxes - foreign | 72429 | 46241 | 24288 | ||

| Income (loss) before income taxes | 260507 | 141885 | 349369 | ||

| Current tax provision (benefit) - federal | 54315 | 52557 | 86623 | ||

| Current tax provision (benefit) - state | 5790 | -1576 | 9866 | ||

| Current tax provision (benefit) - foreign | 60571 | 26918 | 16144 | ||

| Total current tax provision (benefit) | 120676 | 77899 | 112633 | ||

| Deferred tax provision (benefit) - federal | -24383 | -37669 | -10994 | ||

| Deferred tax provision (benefit) - state | -14080 | -17635 | -17794 | ||

| Deferred tax provision (benefit) - foreign | -8384 | -3351 | -1275 | ||

| Total deferred tax provision (benefit) | -46847 | -58655 | -30063 | ||

| Provision for (benefit from) income taxes | 73829 | 19244 | 82570 | ||

| Net income (loss) | 186678 | 122641 | 266799 | ||

| Weighted average shares outstanding - basic | 428822 | 425889 | 420546 | ||

| Weighted average shares outstanding - diluted | 438652 | 436456 | 431893 | ||

| Year end shares outstanding | 430054.212 | 427940.44 | 422910.887 | ||

| Net income (loss) per share - basic | 0.44 | 0.29 | 0.634 | ||

| Net income (loss) per share - diluted | 0.43 | 0.28 | 0.617 | ||

| Number of full time employees | 4500 | 3500 | 2189 | ||

| Number of part time & temporary employees | 200 | 400 | 261 | ||

| Total number of employees | 4700 | 3700 | 2450 | ||

| Number of common stockholders | 290 | 237 | 203 | ||

| Foreign currency translation adjustments | -5464 | -37887 | - | ||

| Geo Holdings Corp (TOK: 2681) | |||||

| Exchange rate used is that of the Year End reported date | |||||

| As Reported Annual Income Statement | |||||

| Report Date | 03/31/2016 | 03/31/2015 | 03/31/2014 | ||

| Currency | JPY | JPY | JPY | ||

| Audit Status | Not Qualified | Not Qualified | Not Qualified | ||

| Consolidated | Yes | Yes | Yes | ||

| Scale | Millions | Millions | Thousands | ||

| Total revenue | 267910 | 270308 | 262324000 | ||

| Cost of sales | -151798 | -157825 | 152301000 | ||

| Gross profit | 116112 | 112483 | 110022000 | ||

| Selling, general & administrative expenses | -99559 | -102925 | 100823000 | ||

| Operating income | 16552 | 9558 | 9198000 | ||

| Interest & dividend income | 49 | 114 | 111000 | ||

| Rental income | 1268 | 1167 | 1193000 | ||

| Other non-operating income | 1043 | 1062 | 453000 | ||

| Total non-operating income | 2361 | 2343 | 1758000 | ||

| Interest expense | -230 | -231 | 332000 | ||

| Rental expenses | -759 | -609 | 595000 | ||

| Transfer to reserve for doubtful account | - | -227 | - | ||

| Other non-operating expenses | -100 | -803 | - | ||

| Total non-operating expenses | -1089 | -1871 | 684000 | ||

| Ordinary income | 17824 | 10030 | 1612000 | ||

| Imapirment loss | -1319 | -1543 | 9344000 | ||

| Other extraordinary losses | -13 | - | 203000 | ||

| Total extraordinary losses | -1333 | -1543 | 203000 | ||

| Income before income taxes | 16491 | 8486 | 1218000 | ||

| Income taxes - current | -5779 | -2074 | 514000 | ||

| Income taxes - deferred | -147 | 925 | 87000 | ||

| Total income taxes | -5927 | -1149 | 1821000 | ||

| Profit | 10563 | 7337 | 7726000 | ||

| Profit attributable to owners of parent | 10563 | 7337 | 4027000 | ||

| Average number of shares outstanding - basic | 51.331 | 53.169 | -39000 | ||

| Average number of shares outstanding - diluted | 51.623 | 53.29 | 3987000 | ||

| Year end shares outstanding | 48.244 | 52.295 | 3738000 | ||

| Earnings per share - basic | 205.78 | 137.99 | -70000 | ||

| Earnings per share - diluted | 204.62 | 137.68 | 3808000 | ||

| Number of full time employees | 3825 | 3579 | 53996.5 | ||

| Number of part time employees | 10421 | 10114 | 54066.499 | ||

| Number of common stockholders | 57105 | 65030 | 53996.5 | ||