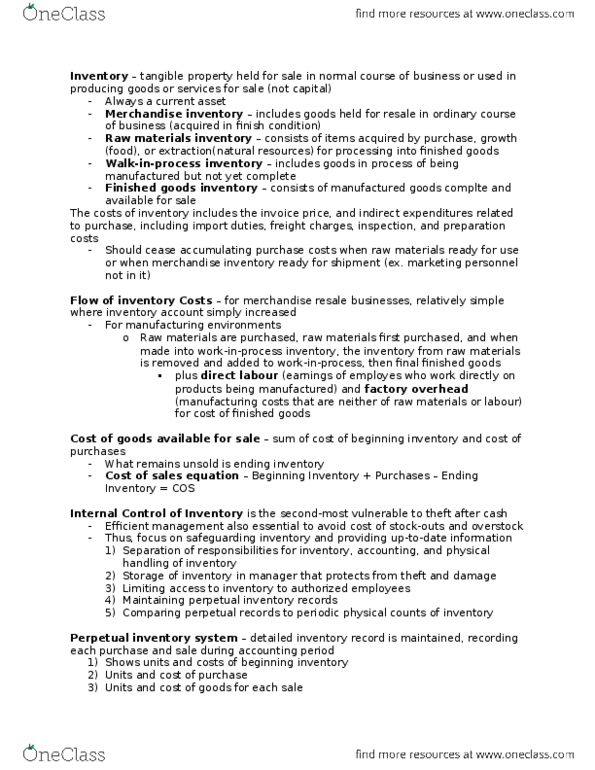

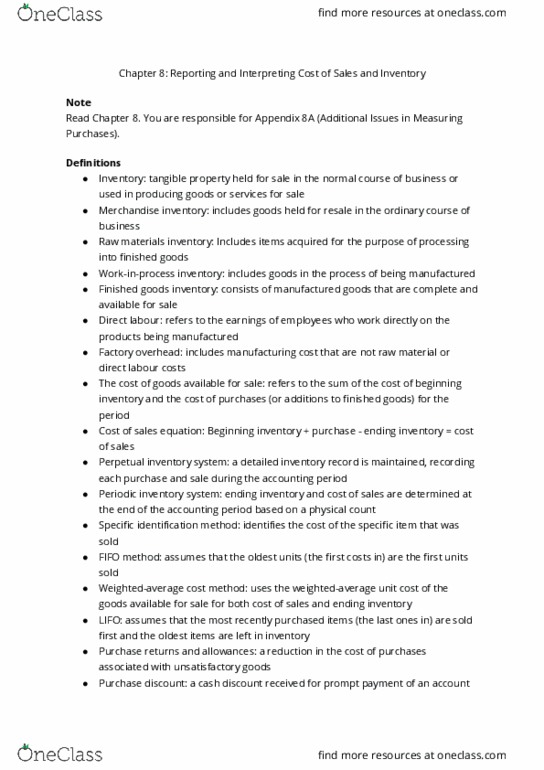

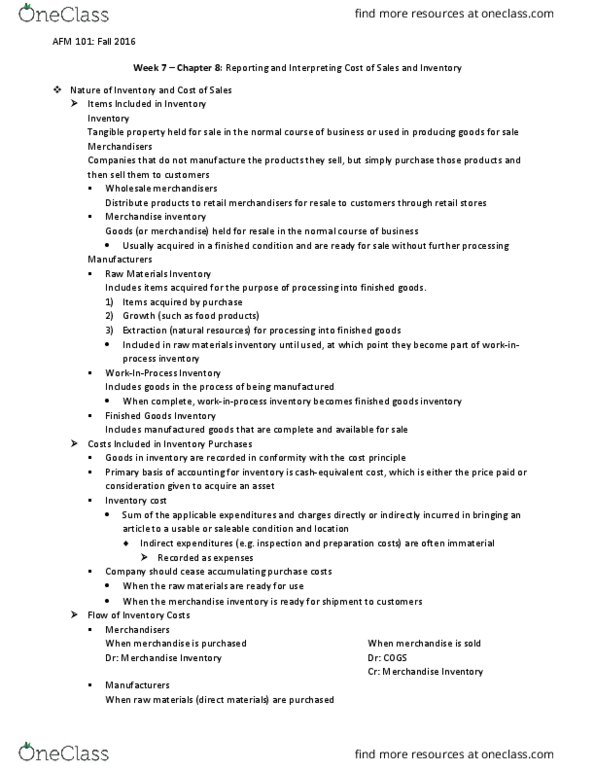

AFM101 Chapter Notes - Chapter 8: Retained Earnings, Inventory Turnover, Perpetual Inventory

Get access

Related Documents

Related Questions

1.) When products held in inventory are sold:

A.)Cost of Goods Sold is credited.

B.)Work in Process Inventory is credited.

C.)Finished Goods Inventory is credited.

D.)Finished Goods Inventory is debited.

2.)Since manufacturing costs (direct materials, direct labor,and overhead) are incurred in the process of manufacturing units ofproduct, these costs are credited t

| A.) | The Direct Materials Inventory, Direct Labor, and ManufacturingOverhead accounts respectively. |

| B.) | Liability accounts. |

| C.) | The Work in Process Inventory account. |

| D.) | The Cost of Goods Sold account. |

3.)Management accounting systems are designed to assistorganizations in the performance of all of the following functionsexcept:

| A.) | The assignment of decision-making authority over companyassets. |

| B.) | Planning and decision-making. |

| C.) | Monitoring, evaluating, and rewarding performance. |

| D.) | The preparation of income tax returns. |

4.)In a schedule of cost of finished goods manufactured, thefigure for total manufacturing costs:

| A.) May be less than the cost of direct materials used. | |

| B.) May be less than the direct labor costs assigned toproduction. | |

| C.) May be less than the manufacturing overhead applied toproduction. | |

| D.) May be less than the cost of finished goodsmanufactured. |

5.) When a manufacturing company purchases raw materials orcomponent parts to be used in manufacturing finished goods, thesecosts are initially debited to:

| A.) Expense accounts. | |

| B.) Raw Materials Inventory. | |

| C.) Finished Goods Inventory. | |

| D.) Manufacturing Overhead. |

6.) The wages paid to employees working directly on a company'sproducts would be shown as a:

| A.) Credit to Direct Labor. | |

| B.) Debit to Direct Labor. | |

| C.) Credit to Work in Process. | |

| D.) Debit to Manufacturing Overhead. |

7.) Amounts credited to the Work in Process inventory accountmay best be described as:

| A.) The cost of finished goods manufactured. | |

| B.) Total manufacturing costs charged to production. | |

| C.) The cost of goods sold. | |

| D.) Direct materials purchased, direct labor costs paid, andpayments for items classified as manufacturing overhead. |

Problem 15-1A Production costs computed and recorded; reports prepared LO C2, P1, P2, P3, P4

[The following information applies to the questions displayed below.]

Marcelino Co.'s March 31 inventory of raw materials is $82,000. Raw materials purchases in April are $580,000, and factory payroll cost in April is $381,000. Overhead costs incurred in April are: indirect materials, $59,000; indirect labor, $25,000; factory rent, $31,000; factory utilities, $24,000; and factory equipment depreciation, $58,000. The predetermined overhead rate is 50% of direct labor cost. Job 306 is sold for $650,000 cash in April. Costs of the three jobs worked on in April follow.

| Job 306 | Job 307 | Job 308 | ||||||||||

| Balances on March 31 | ||||||||||||

| Direct materials | $ | 28,000 | $ | 36,000 | ||||||||

| Direct labor | 24,000 | 15,000 | ||||||||||

| Applied overhead | 12,000 | 7,500 | ||||||||||

| Costs during April | ||||||||||||

| Direct materials | 139,000 | 205,000 | $ | 100,000 | ||||||||

| Direct labor | 103,000 | 152,000 | 101,000 | |||||||||

| Applied overhead | ? | ? | ? | |||||||||

| Status on April 30 | Finished (sold) | Finished (unsold) | In process | |||||||||

rev: 03_15_2018_QC_CS-121813

Problem 15-1A Part 1

Required:

1. Determine the total of each production cost incurred for April (direct labor, direct materials, and applied overhead), and the total cost assigned to each job (including the balances from March 31).

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Problem 15-1A Part 2

- Materials purchases (on credit).

- Direct materials used in production.

- Direct labor paid and assigned to Work in Process Inventory.

- Indirect labor paid and assigned to Factory Overhead.

- Overhead costs applied to Work in Process Inventory.

- Actual overhead costs incurred, including indirect materials. (Factory rent and utilities are paid in cash.)

- Transfer of Jobs 306 and 307 to Finished Goods Inventory.

- Cost of goods sold for Job 306.

- Revenue from the sale of Job 306.

- Assignment of any underapplied or overapplied overhead to the Cost of Goods Sold account. (The amount is not material.)

2. Prepare journal entries for the month of April to record the above transactions.

Problem 15-1A Part 3

3. Prepare a schedule of cost of goods manufactured.

| |||||||||||||