AFM102 Chapter Notes - Chapter 7: Contribution Margin, Fixed Cost, Variable Cost

21 Nov 2013

School

Department

Course

Professor

Document Summary

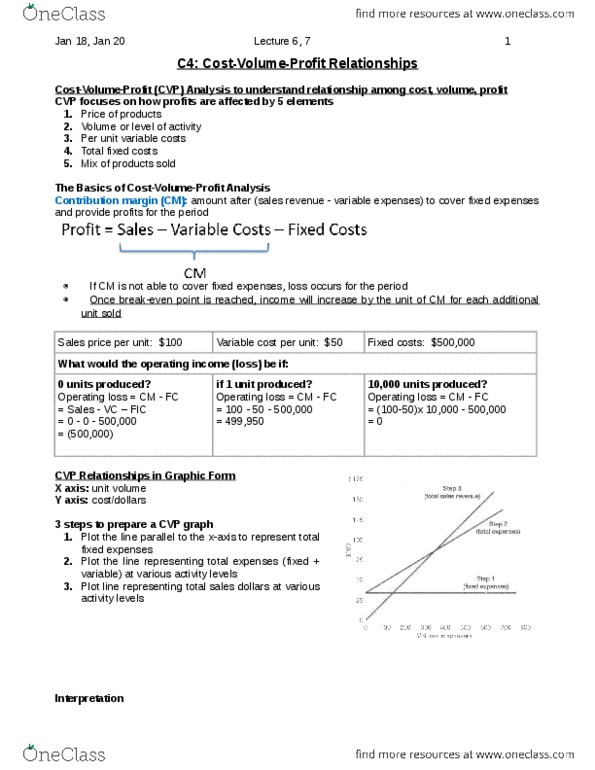

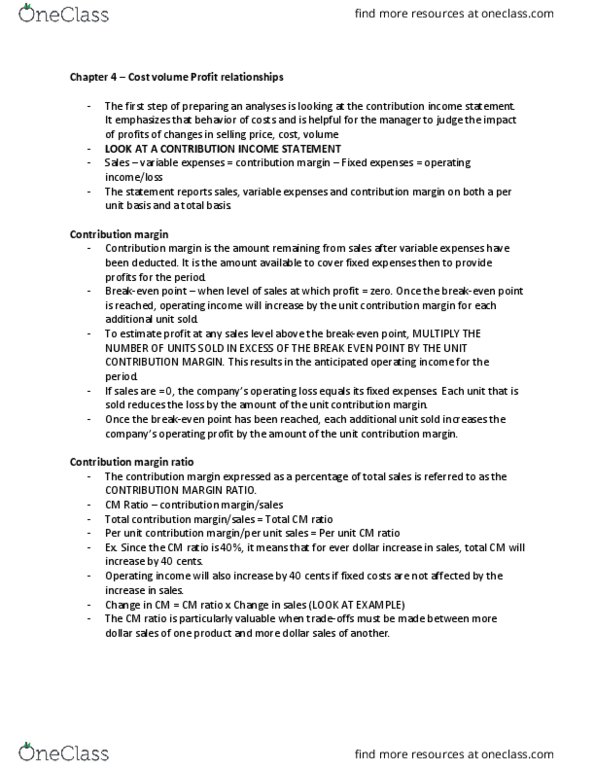

Cvp analysis is a powerful tool that helps managers understand the relationships among cost, volume, and profit focuses on: prices of products, volume/level of activity, per unit variable cost, tfc and mix of products sold. Cvp relationships in graphic form cost-volume-profit graph: the relationships among revenues, costs and level of activity in an organization presented in graphic form. Break-even point is where the total revenue and total expenses cross profit is the area above the break-even point (between total rev. and total exp) and loss is the area below. Contribution margin (cm) ratio contribution (cm) ratio: the contribution margin as a percentage of total sales. X = break-even point in units sold profit = (sales variable expenses) fixed expenses sales = variable expenses + fixed expenses + profits. Target operating profit analysis contribution margin approach: x = (fixed exp + target profit) / unit contribution margin.