AFM102 Chapter Notes - Chapter 5: Cost Driver, Expense, Product Design

21 Nov 2013

School

Department

Course

Professor

Document Summary

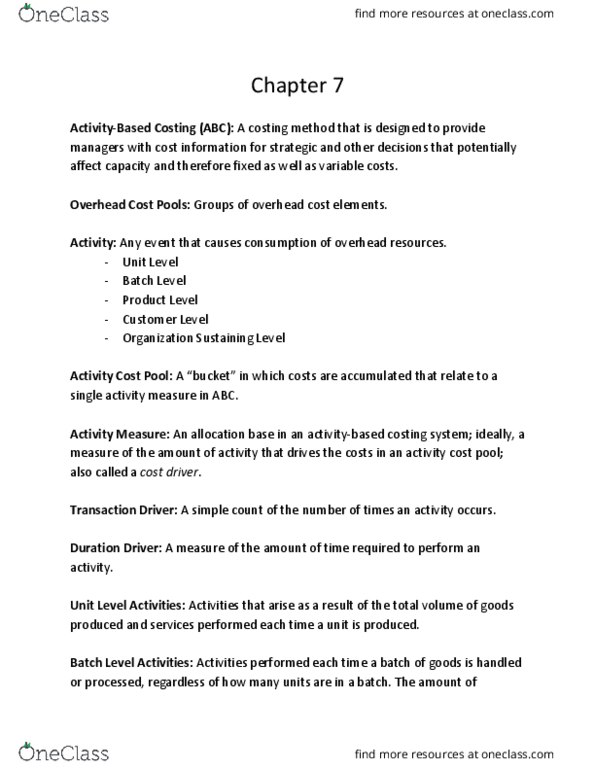

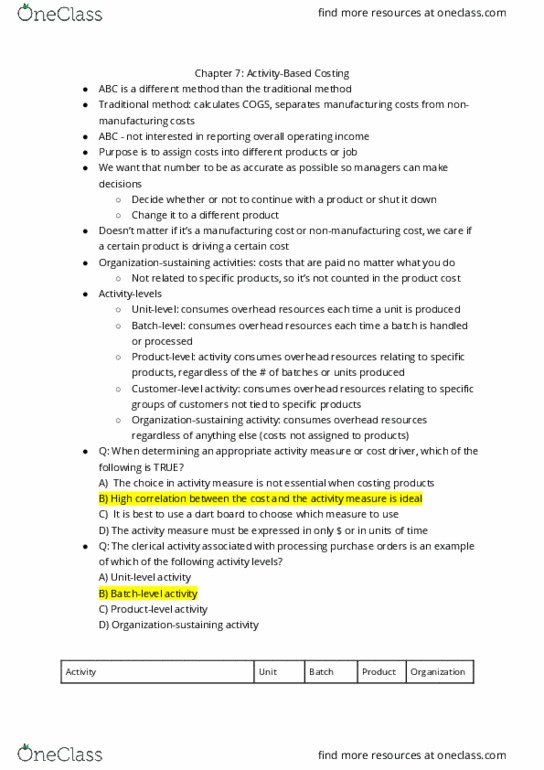

Chapter 5: activity-based costing activity-based costing (abc): a costing method based on activities that is designed to provide managers with cost information for strategic and other decisions that potentially affect capacity and therefore fixed costs. Duration driver: a measure of the amount of time required to perform an activity. The cost of idle capacity in activity-based costing costs of idle capacity are not charged to products page 1 of 5. Designing an activity-based costing system initiative to implement abc must be strongly supported by top management. Managers might not see a reason to change without leadership from top management if top management doesn"t support then, subordinates will quickly get the message that abc is not important and will abandon its. Design and implementation of an abc system should be the responsibility of cross-functional team (not the accounting dept) cost object: the specific product or service to be costed.