AFM481 Chapter Notes -Operating Leverage, Variable Cost, Fixed Cost

6 Nov 2013

School

Department

Course

Professor

Document Summary

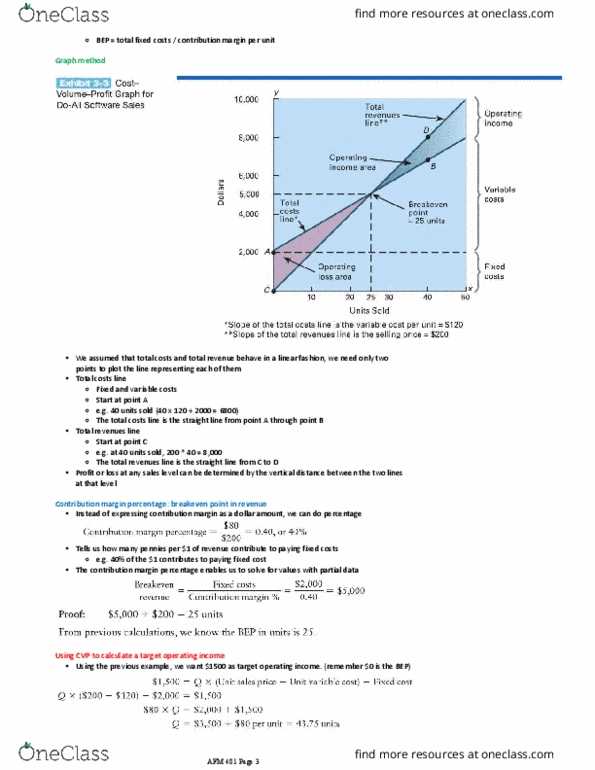

To examine changes in profits in response to changes in sales volumes, cost and prices. Contribution margin = total revenue total variable cost. Contribution margin (cmu) = selling price per unit variable cost per unit. Earnings before tax (ebt) = (selling price variable cost) quantity fixed costs. Assume that fixed costs, selling price and variable costs are constant. We can use the formula to solve for q. This will give us quantity required to achieve our target profit (ebt) Q = (fixed costs + ebt) / cmu. Contribution margin ratio (cmr) is the % of the selling price per unit over the variable cost per unit. Cmr = (s v) / s for a single unit. Selling price q (revenue) = (fixed costs + ebt) / cmr. Level of operating activity so that sales revenue = 0. We went to set ebt = 0. Breakeven quantity is the q that will make ebt = 0.