ACTSC371 Chapter Notes - Chapter 5: Risk Premium, Risk Neutral, Standard Deviation

14 Apr 2016

School

Department

Course

Professor

Document Summary

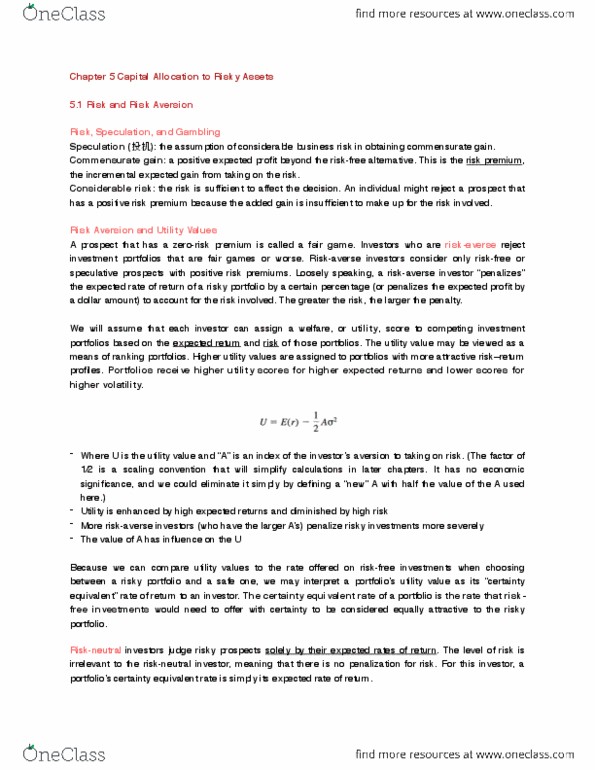

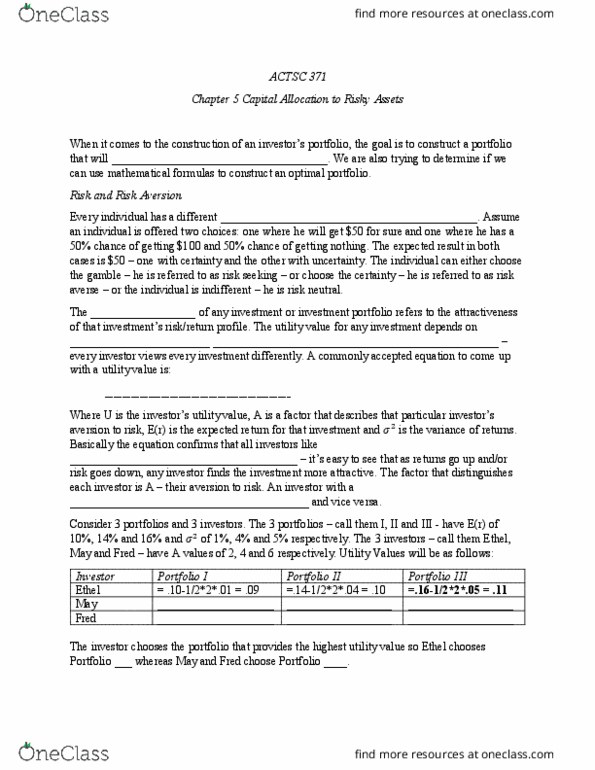

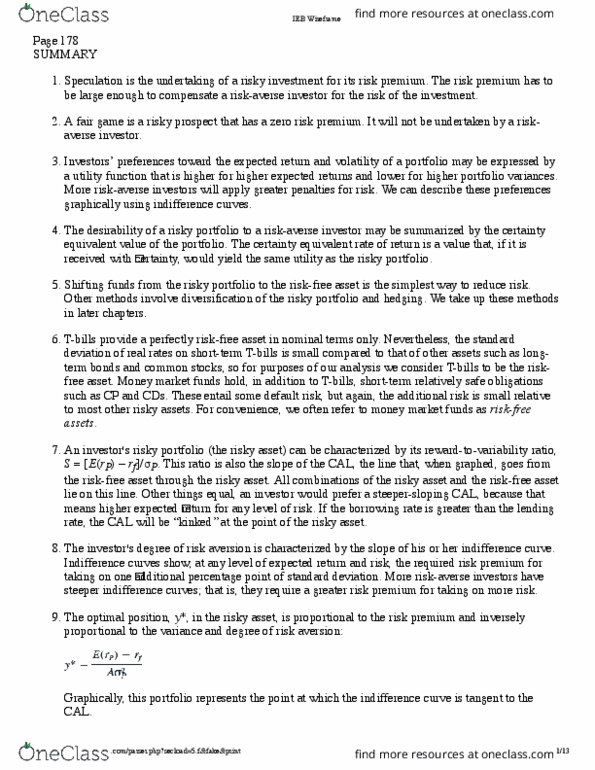

The trade-of between risk and return of a potenial investment porfolio. Judge risky prospects solely by their expected rates of return. Certainty equivalent rate = expected rate of return. Mean-variance criterion: consider 2 porfolios a & b with respecive expected returns mew(a) & mew(b) and standard deviaion of returns sigma(a) & sigma(b) Risk is measured by the standard deviaion: mean-variance (m-v) criterion: Porfolio a is said to dominate (or is preferred to) b if. And at least 1 inequality is strict (rule out diference) U = e(r) ( )a(sigma)^2: u = uility, e(r) = expected return on the asset or porfolio, a = coeicient of risk aversion, sigma^2 = variance of returns. Characterisics of the quadraic uility: u increases with expected return, u can be an increasing, decreasing, or a constant, funcion in volaility depending on the sign of a.