AFM101 Chapter Notes - Chapter 3: Accrual, Asset

15 Jun 2018

School

Department

Course

Professor

Chapter 3

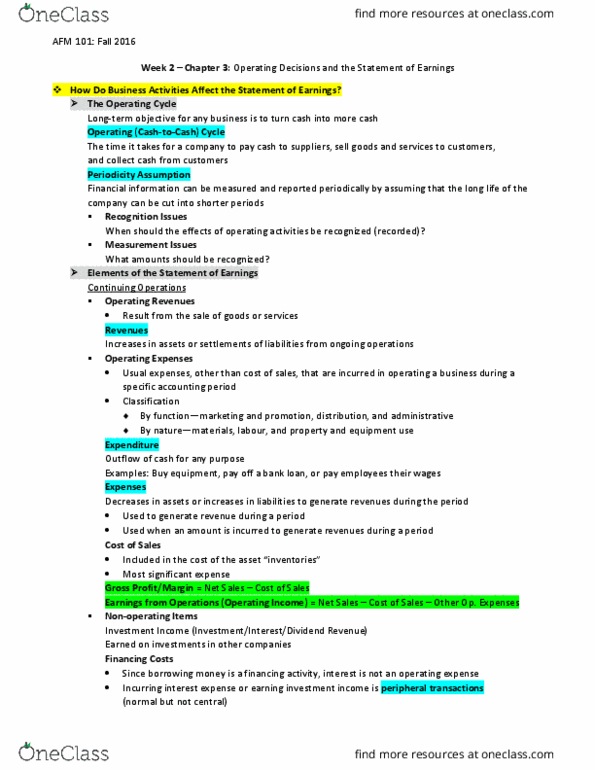

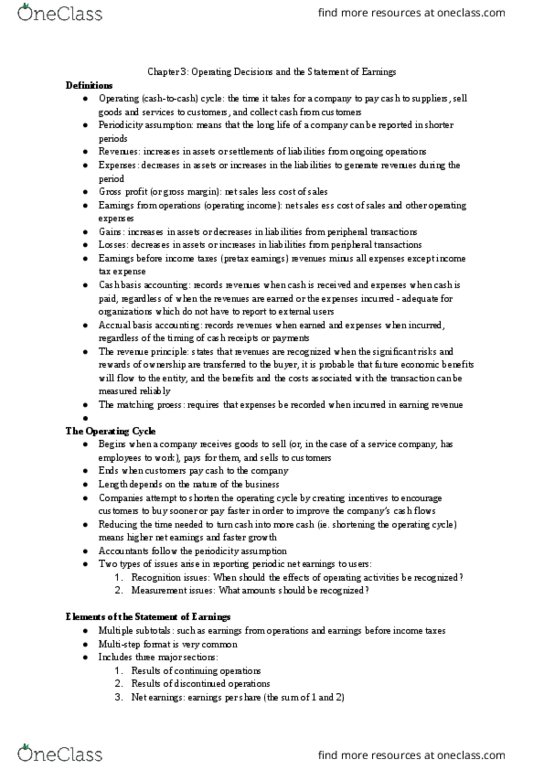

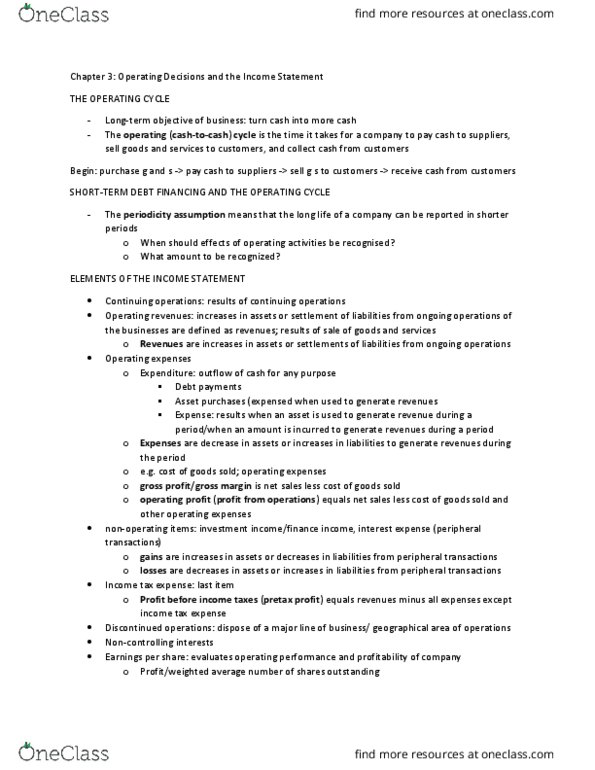

Operating (Cash to Cash) Cycle: The time it takes for a company to pay

cash to suppliers, sell good and services to customers, and collect cash

from customers.

The Periodicity Assumption: Means that the long life of a company can

be reported in shorter periods.

Revenues: Increases in assets or settlements of liabilities from ongoing

operations.

Expenses: Decreases in assets or increases in liabilities to generate

revenues during the period.

Gross Profit: Net sales less cost of sales.

Earnings From Operations: Equals net sales less cost of sales and

other operating expenses.

Non-operating Expenses and Income: Includes investment income,

financing costs, or gains or losses on disposal of assets.

Gains: Increases in assets or decreases in liabilities from peripheral

transactions.

Losses: Decreases in assets or increases in liabilities from peripheral

transactions.

Earnings Before Income Tax: Equals revenues minus all expenses

except income tax expense.

Discontinued Operations: Are presented separately from the results of

continuing operations.

Cash Basis Accounting: Records revenues when cash is received and

expenses when cash is paid.

find more resources at oneclass.com

find more resources at oneclass.com

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Operating (cash to cash) cycle: the time it takes for a company to pay cash to suppliers, sell good and services to customers, and collect cash from customers. The periodicity assumption: means that the long life of a company can be reported in shorter periods. Revenues: increases in assets or settlements of liabilities from ongoing operations. Expenses: decreases in assets or increases in liabilities to generate revenues during the period. Gross profit: net sales less cost of sales. Earnings from operations: equals net sales less cost of sales and other operating expenses. Non-operating expenses and income: includes investment income, financing costs, or gains or losses on disposal of assets. Gains: increases in assets or decreases in liabilities from peripheral transactions. Losses: decreases in assets or increases in liabilities from peripheral transactions. Earnings before income tax: equals revenues minus all expenses except income tax expense. Discontinued operations: are presented separately from the results of continuing operations.