AFM101 Chapter 9: AFM 101 chapter 9 notes.2

26 Jun 2018

School

Department

Course

Professor

AFSA Education

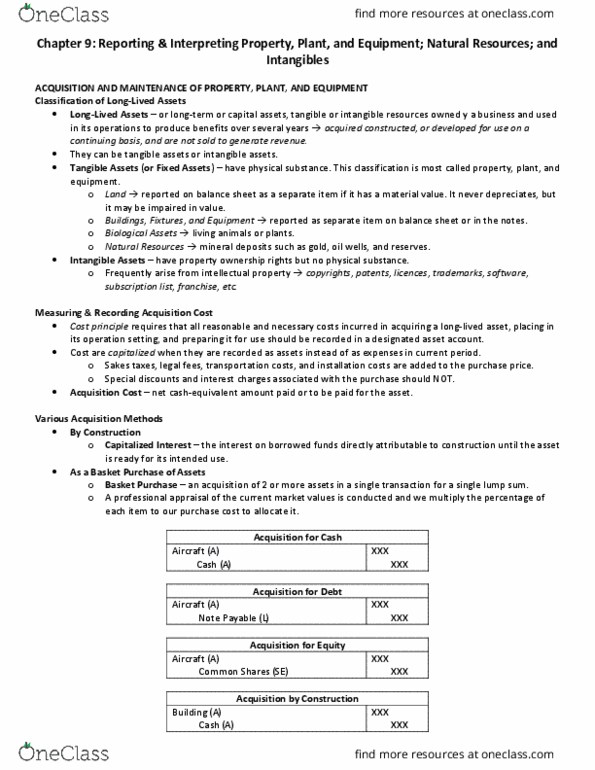

o Capitalized interest: represents interest on borrowed funds directly attributable to

construction until the asset is ready for its intended use

o Building (A)

Cash (A)

As a Basket Purchase of Assets

o Basket purchase: an acquisition of two or more assets in a single transaction for a single

lump sum

Cost of each asset must be measured and recorded separately

o

o Ratio of market value x total cost = cost of asset

Repairs, Maintenance, and Betterments

Expenditure: payment of money to acquire g or s

Expenditures that are made after an asset is acquired are classified as:

1. Ordinary repairs and maintenance, or revenue expenditures

i. Extraordinary repairs and maintenance = expenditures for normal operating upkeep

of long-lived assets

ii. Revenue expenditures: maintain the productive capacity of the asset during the

current accounting period only and are recorded as expenses

2. Extraordinary repairs and betterments

i. Extraordinary repairs: infrequent expenditures that increase the asset's economic

usefulness in the future

ii. Betterments: costs incurred to enhance the productive or service potential of a long-

lived asset

iii. Capital expenditures: increase the productive life, operating efficiency, or capacity of

the asset and are recorded as increases in asset accounts, not as expenses

Use, Impairment, and Disposal of PP&E

Depreciation Concepts

Depreciation: process of allocating the acquisition cost of buildings and equipment over their

useful lives by using a systematic and rational method

Depreciation expense

Accumulated depreciation

Carrying amount (or book value): acquisition cost of an asset less accumulated depreciation and

any write-downs in asset value

o

Calculation of depreciation expense requires three amounts:

o Acquisition cost

o Estimated useful life to the company

o Estimated residual (or salvage) value at the end of the asset's useful life to the company

Two of three amounts are estimates, therefore, depreciation expense is an estimate

o Estimated useful life: the expected service life of an asset to the current owner

Must conform to the continuity assumption (businesses will continue to pursue its

commercial objectives and will not liquidate in the foreseeable future)

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Afsa education: capitalized interest: represents interest on borrowed funds directly attributable to construction until the asset is ready for its intended use, building (a) As a basket purchase of assets lump sum: basket purchase: an acquisition of two or more assets in a single transaction for a single. Cost of each asset must be measured and recorded separately: ratio of market value x total cost = cost of asset. Expenditure: payment of money to acquire g or s. Expenditures that are made after an asset is acquired are classified as: ordinary repairs and maintenance, or revenue expenditures, extraordinary repairs and betterments. Extraordinary repairs and maintenance = expenditures for normal operating upkeep of long-lived assets. Revenue expenditures: maintain the productive capacity of the asset during the current accounting period only and are recorded as expenses. Extraordinary repairs: infrequent expenditures that increase the asset"s economic usefulness in the future.