AFM102 Chapter Notes - Chapter 5: Expense, Income Statement, Finished Good

27 Jan 2018

School

Department

Course

Professor

Document Summary

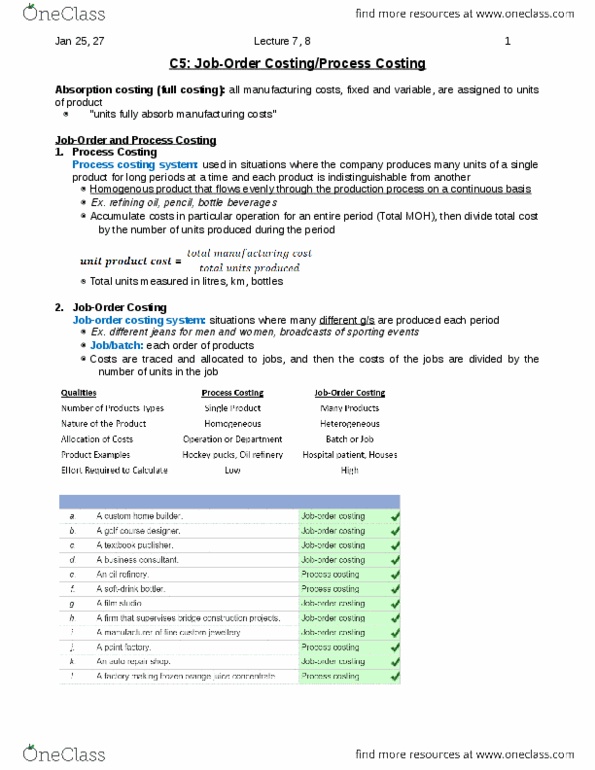

Absorption costing, aka full costing all manufacturing costs, fixed and variable, are assigned to units of production, units fully absorb manufacturing costs. Source data gets posted on a computerized system and can be posted to job cost sheets. Ra(cid:449) materials i(cid:374)(cid:448)e(cid:374)tor(cid:455) (cid:894)+a(cid:895) (cid:454)(cid:454)(cid:454: labour cost. Salaries a(cid:374)d wages pa(cid:455)a(cid:271)le (cid:894)+l(cid:895) (cid:454)(cid:454)(cid:454: only direct labour is added to the work in process account, direct labour costs are added to work in process and the individual job cost sheets. Labour costs added to manufacturing overhead represent indirect labour costs: manufacturing overhead costs, directly entered into the manufacturing overhead account as they are incurred. A(cid:272)(cid:272)ou(cid:374)ts pa(cid:455)a(cid:271)le (cid:894)+l(cid:895) (cid:454)(cid:454)(cid:454: all manufacturing overhead costs are directly recorded as they are incurred day by day throughout the period. The application of manufacturing overhead: the manufacturing overhead account operates as a clearing account, at certain intervals over the year, overhead cost gets transferred from the manufacturing.