AFM102 Chapter Notes - Chapter 6: Indian Railways, Finished Good, Production Schedule

31 Jan 2018

School

Department

Course

Professor

Document Summary

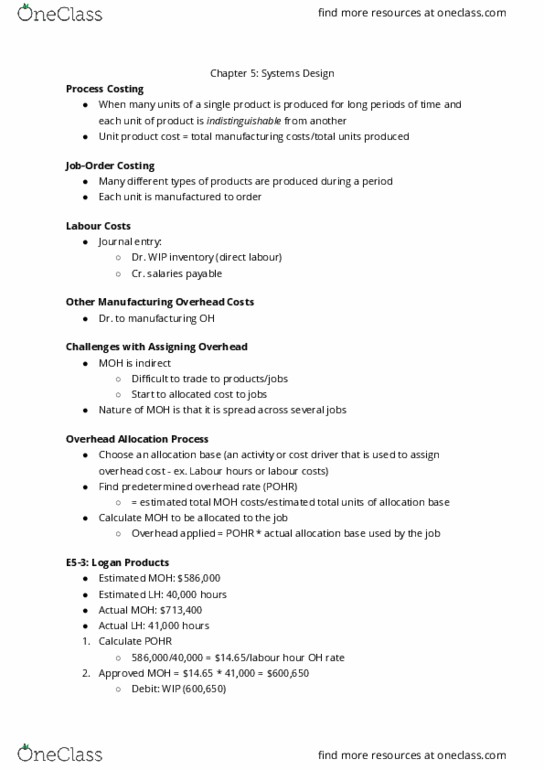

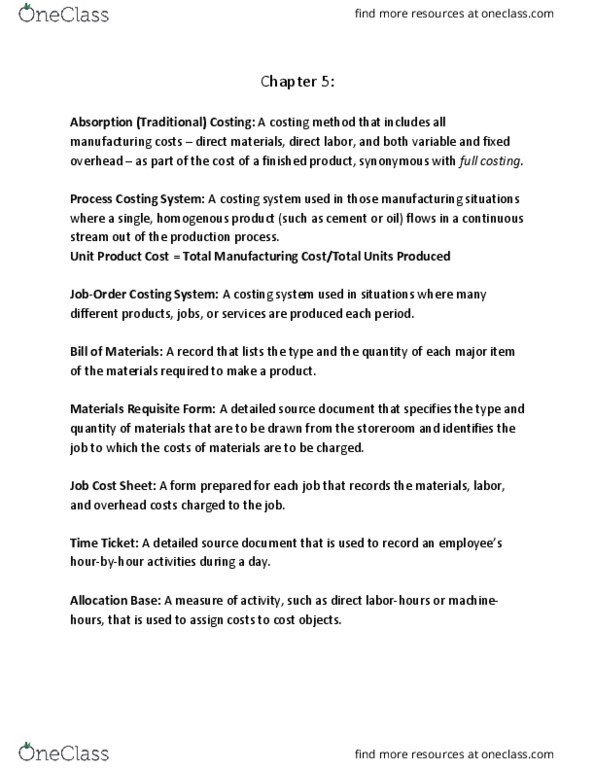

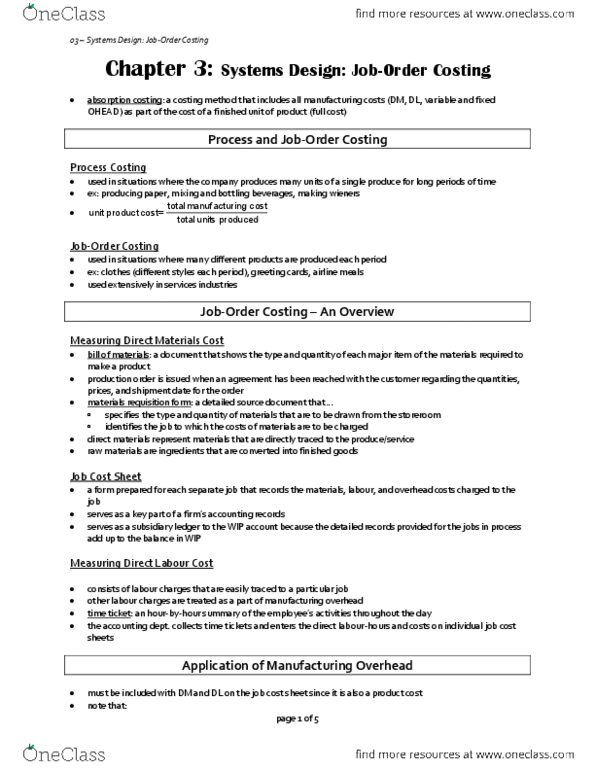

Same basic purposes: assign materials, labour, and overhead costs to products and provide a mechanism for computing unit costs. Same basic manufacturing accounts: manufacturing overhead, raw materials, wip, finished goods. Flow of costs in manufacturing accounts is the same. Summarizes number of units moving through the department in a period. Shows what costs were charged to a department and how they were disposed. Journal entry to record materials using in other processing departments. Ra(cid:449) (cid:373)aterials xxx: labour costs, traced to departments, not individual jobs. Ma(cid:374)ufacturi(cid:374)g o(cid:448)erhead xxx: completing the cost flows, product units are transferred to the next department for further processing when completed, transfer costs of partially completed units from one department to another. Wip mixi(cid:374)g xxx: costs of completed units are transferred to the finished goods inventory account. Wip filli(cid:374)g xxx: customer" order is filled and units are sold. Weighted-average method: equivalent units of production = units transferred to the next department or to finished goods +