AFM102 Chapter Notes - Chapter 2: Balance Sheet, Wags, Fixed Cost

16 Jan 2016

School

Department

Course

Professor

Document Summary

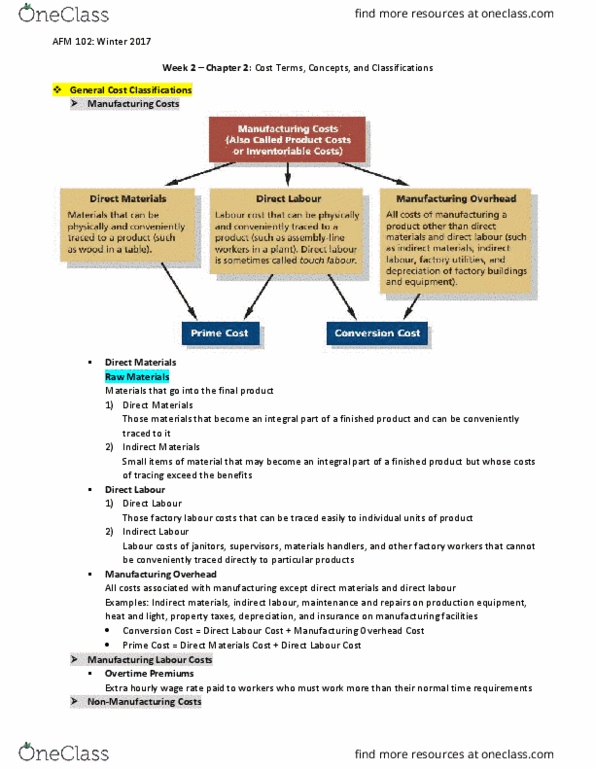

3 broad categories of manufacturing costs (crucial to production, put it in inventory asset: direct materials. Direct materials: materials that go into the finished product and can be physically and conveniently traced to it. Ex. seats bombardier purchases from subcontractors to install in its passenger trains, radio installed in a car, the engine. Raw materials: any materials that go into the final product/ used in final product. Not only unprocessed natural resources like wood pulp. Note: the finished product of one company can become the raw materials of another company o. Ex. car batteries produced by magma are a raw material used by bmw in cars : direct labour. Direct labour: labour costs that can be easily traced to the individual units of product; charged by hour. Ex. wages paid to automobile assembly workers: manufacturing overhead. Manufacturing overhead (indirect manufacturing cost, factory overhead, factory burden): all costs associated with operating the production facility (no direct materials and direct labour)