AFM273 Chapter Notes - Chapter 10: Confidence Interval

26 Jun 2018

School

Department

Course

Professor

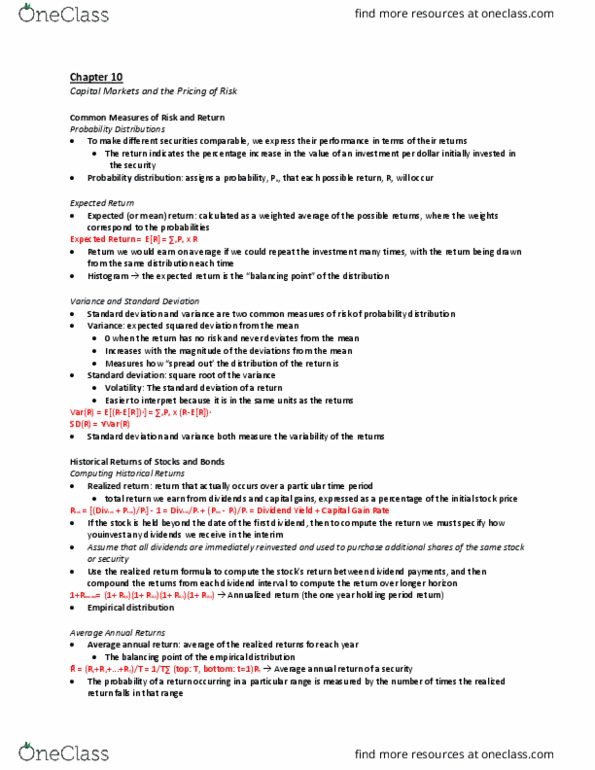

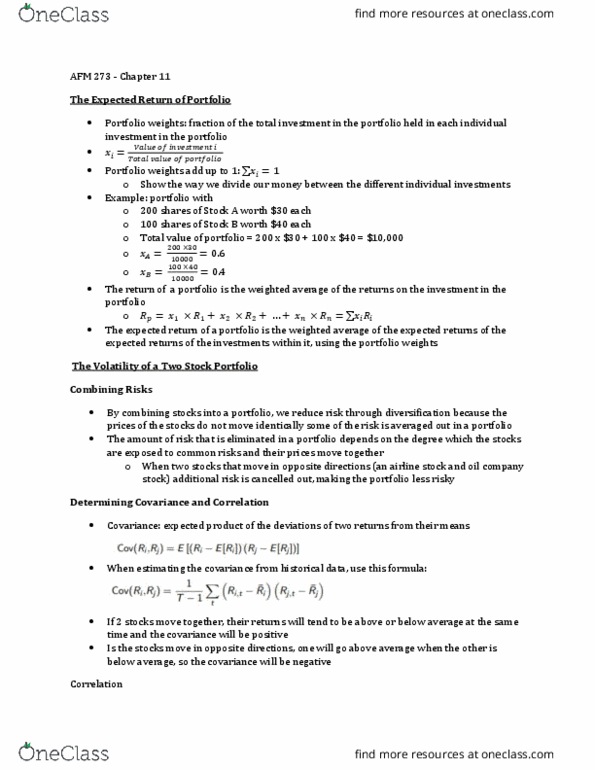

Chapter 10

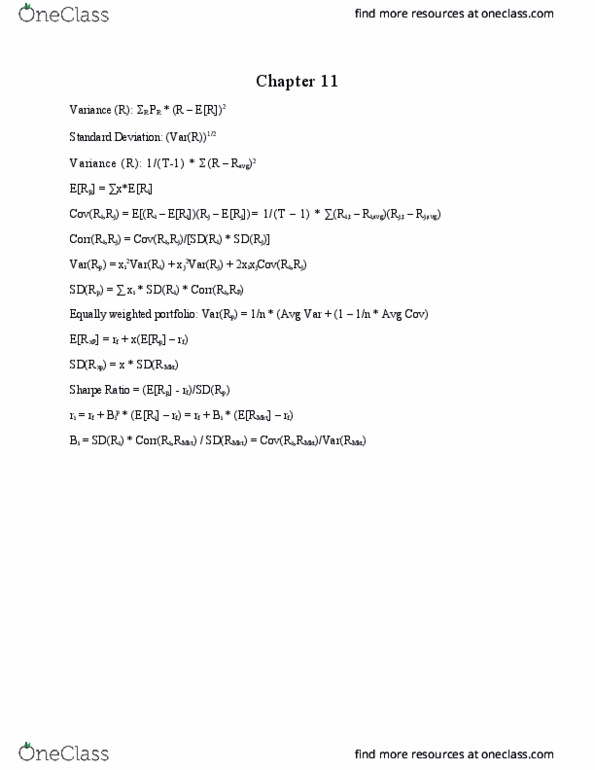

Variance (R): ΣR PR * (R – E[R])2

Standard Deviation: (Var(R))1/2

Variance (R): 1/(T-1) * Σ (R – Ravg)2

Standard Error: SD/(# of observations)1/2 = volatility/(# of returns)1/2

95% Confidence Interval: Avg Return +/- 2(Standard Error)

Beta: The expected percent change in the excess return of a security for a 1%

change in the excess return of the market portfolio.

Market Risk Premium = E[RMk t ] - rf

E[ri] = Risk-Free Rate + Risk Premium = r f + Bi * (E[RM k t ] – rf)

find more resources at oneclass.com

find more resources at oneclass.com