AFM273 Chapter 9: Chapter 9 - AFM 273.docx

75 views6 pages

17 Feb 2015

School

Department

Course

Professor

Document Summary

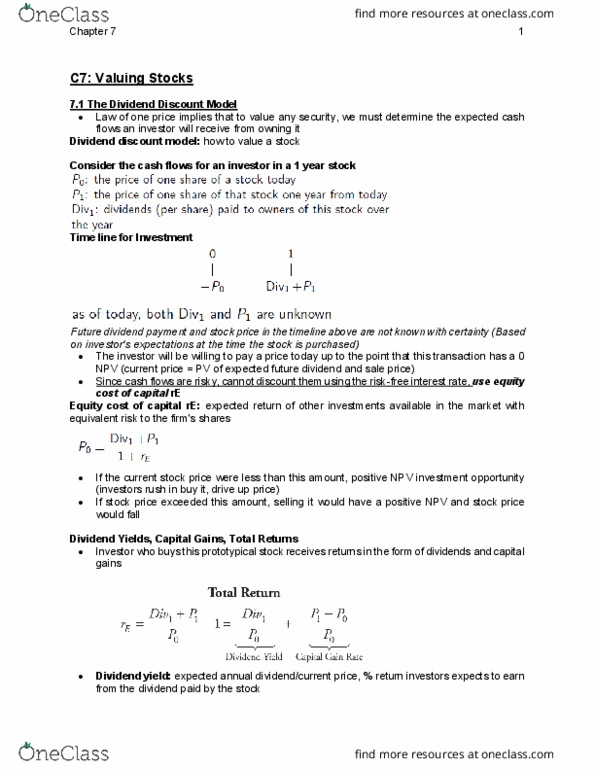

+ div2 (1+ )2 + + divn (1+ ) n + pn (1+ )n: this is the dividend discount model. Dividend payout rate: assuming number of shares outstanding is constant, firms can do three things to increase its dividend, increase earnings (net income, increase dividend payout rate, decrease shares outstanding, firm can do one of two things with earnings, pay them out to investors, retain and reinvest them, change in earnings = new investment x return on new investment, new investment = earnings x retention rate, retention rate is the fraction of current earnings that the firm retains, earnings growth rate = change in earnings / earnings = retention rate x return on new investment g = retention rate x return on new investment, if firm keeps retention rate constant, then growth rate in dividends will equal growth rate of earnings.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

The discounted dividend model can be used to value divisions and firms that do not pay dividends. For the discounted dividend model, a firm's weighted average cost of capital is used as the discount rate. For the corporate valuation model, a firm's cost of equity is used as the discount rate. |

For the constant growth model to hold, a firm's cost of equity needs to be greater than its constant dividend growth rate (i.e., rs > g). From the constant growth model, if the constant dividend growth rate is equal to zero, a firm's share price is equal to the constant dividend divided by the cost of equity (i.e., g=0). If a company's constant dividend growth rate is negative, the formula for the constant growth model cannot be applied. |

The internal rate of return method (IRR) assumes that cash flows are reinvested at the internal rate of return. The modified internal rate of return method (MIRR) assumes that cash flows are reinvested at the weighted average cost of cpaital. For mutually exclusive projects, if there is a conflict between NPV and IRR, the project with the highest IRR is chosen. The IRR is independent of a firm's weighted average cost of capital. |

The WACC only represents the "hurdle rate" for a typical project with average risk. Therefore, the project's WACC should be adjusted to reflect the project's risk. Firms with riskier projects generally have a lower WACC. Holding all else constant, an increase in the target debt ratio tends to lower the WACC. |

Short-term bond prices are less sensitive than long-term bond prices to interest rate changes. Companies are not likely to call bonds unless interest rates have declined significantly. Thus, the call provision is valuable to firms but detrimental to long term investors. On balance, bonds that have a sinking fund are regarded as being safer than those without such a provision. |

If beta < 1.0, the security is less risky than average. According to the Security Market Line (SML), in general, a companyâs expected return will double when its beta doubles. According to the Security Market Line (SML), if a portfolio of real world stocks has a beta of zero, the required rate of return for the portfolio is equal to the risk-free rate. |

7.37%. 11.05%. 8.32%. |

It ignores cash flows occurring after the payback period. It ignores the time value of money, that is, dollars received in different years are all given the same weight. |

1.82. 2.00. 1.94 |

undervalued. overvalued. |

13.92%. 16.34%. 12.17%. |

$221.86. $195.23. $257.35. |

10.82%. 11.76%. 9.64%. |

10 years. 4.58 years. 6.12 years. |

12.04%. 14.93%. 9.15%. |

1.24 years. 1.62 years. 1.15 years.

|