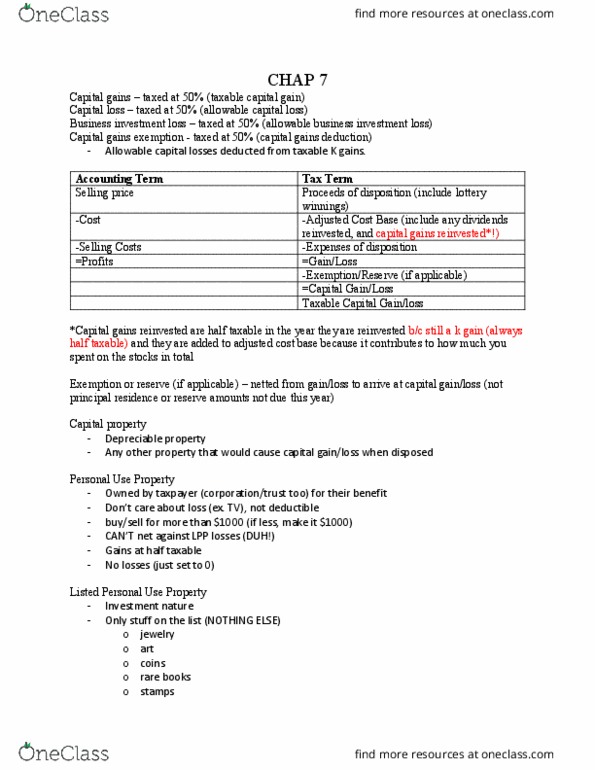

AFM362 Chapter Notes - Chapter 7: Real Estate Transfer Tax

Get access

Related Documents

Related Questions

Ted and Marge Dean are married and always have lived in a community property state. Ted (age 92) suffers from numerous disorders and is frequently ill, while Marge (age 70) is in good health. The Deans currently need $500,000 to meet living expenses, make debt payments, and pay Ted's backlog of medical expenses. They are willing to sell any one of the following assets.

| Adjusted Basis | FairMarket Value | |

| a. Wren Corporation Stock | 200,000 | 500,000 |

| b. Gull Corporation Stock | 600,000 | 500,000 |

| c. Unimproved Land | 650,000 | 500,000 |

The stock investments are part of the Deans' community property, while the land is Ted's separate property that he inherited from his mother. If the land is not sold, Ted is considering making a gift of it to Marge.

a. Complete a letter to the Deans advising them on these matters.

Dear Mr. and Mrs. Dean: Regarding the matter we recently discussed about the disposition of various assets, I suggest the following. ⢠Keep the stock in Wren Corporation, because its income tax basis will increase to $ 500,000 upon the death of either of you. This way, the survivor will have $ 300,000 less income to recognize when the stock is sold. ⢠Ted should make a gift of the land to Marge. No gift tax results from the gift, and Marge will have a basis for gain of $ ????? . Her basis for loss is $ 500,000 . If Marge inherited the land, her basis for both the gain and loss would be $ 500,000 . ⢠The stock in Gull Corporation should be sold. The resulting $ 100,000 capital loss can be applied against capital gains and the excess deducted against regular income up to $ ????? per year. One-half of any unused loss remaining should one of you predecease the other can be used by the survivor. Consequently, the transactions summarized above improve your present and future income tax positions while providing the $ 500,000 cash that you need to meet expenses. If I can be of further assistance to you in this matter, please contact me. Sincerely, Laura Sims, CPA Manager