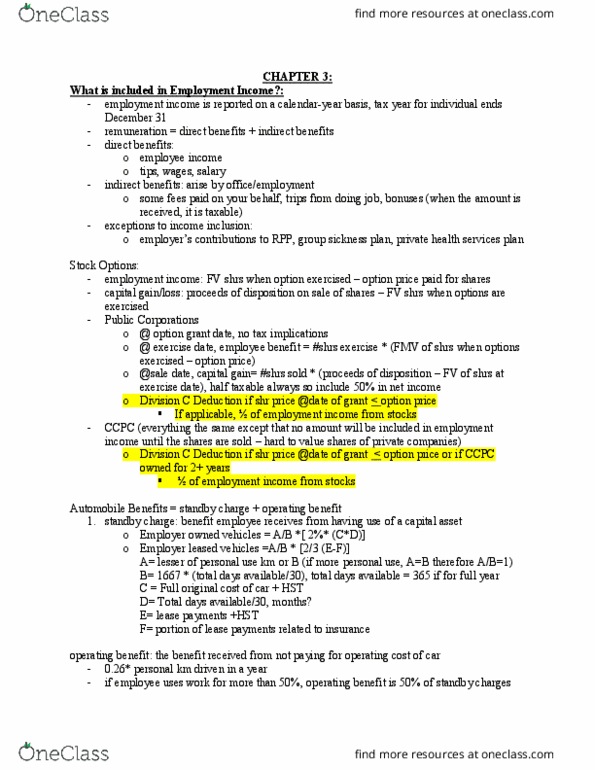

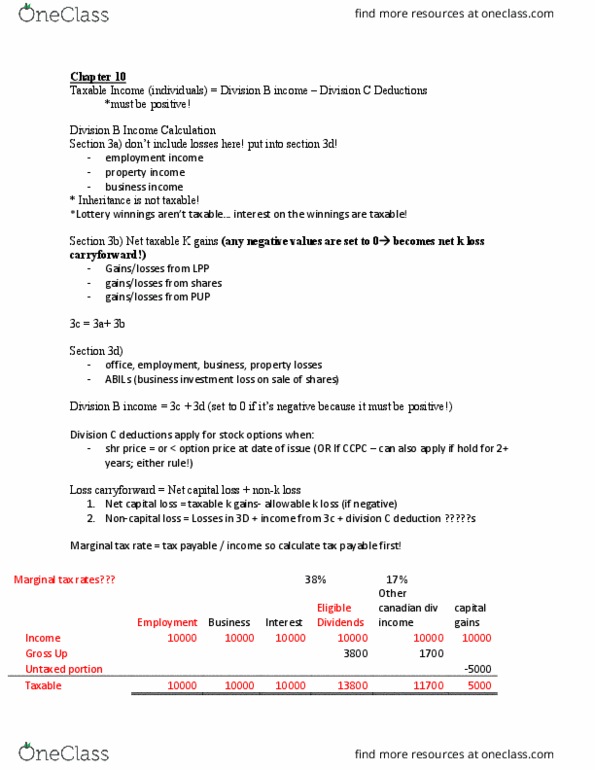

Choose the correction answer

7. Stock warrants outstanding shouldbe classified as

a. liabilities.

b. reductions of capital contributed in excess ofpar value.

c. assets.

d. None of these answers are correct.

8. The date on which to measure thecompensation element in a stock option granted to a corporateemployee ordinarily is the date on which the employee

a. is granted the option.

b. has performed all conditions precedent toexercising the option.

c. may first exercise the option.

d. exercises the option.

9. Which of the following isnot a characteristic of a noncompensatory stockpurchase plan?

a. It is open to almost all full-time employees.

b. The discount from market price is small.

c. The plan offers no substantive optionfeature.

d. All of these are characteristics.

10. On January 1, 2014, Trent Companygranted Dick Williams, an employee, an option to buy 400 shares ofTrent Co. stock for $30 per share, the option exercisable for 5years from date of grant. Using a fair value option pricing model,total compensation expense is determined to be $3,600. Williamsexercised his option on September 1, 2014, and sold his 400 shareson December 1, 2014. Quoted market prices of Trent Co. stock during2014 were:

January1 $30 per share

September1 $36 per share

December1 $40 per share

The service period is for two years beginning January 1, 2014. As aresult of the option granted to Williams, using the fair valuemethod, Trent should recognize compensation expense for 2014 on itsbooks in the amount of

a. $4,000.

b. $3,600.

c. $1,800.

d. $0.

11. Incomputing earnings per share for a simple capital structure, if thepreferred stock is cumulative, the amount that should be deductedas an adjustment to the numerator (earnings) is the

a. preferred dividends in arrears.

b. preferred dividends in arrears times (one minusthe income tax rate).

c. annual preferred dividend times (one minus theincome tax rate).

d. None of these answers are correct.

12. The following information isavailable for Barone Corporation:

January 1,2015 Sharesoutstanding 2,000

April 1,2015 Sharesissued 320,000

July 1,2015 Treasury sharespurchased 120,000

October 1,2015 Shares issued in a 100%stockdividend 2,200

The number of shares to be used incomputing earnings per common share for 2015 is

a. 4,520,800.

b. 4,380,000.

c. 4,360,000.

d. 2,730,000.

13. Incomputing earnings per share, the equivalent number of shares ofconvertible preferred stock are added as an adjustment to thedenominator (number of shares outstanding). If the preferred stockis cumulative, which amount should then be added as an adjustmentto the numerator (net earnings)?

a. Annual preferred dividend

b. Annual preferred dividend times (one minus theincome tax rate)

c. Annual preferred dividend times the income taxrate

d. Annual preferred dividend divided by the incometax rate

14. Fugate Company had 900,000 sharesof common stock issued and outstanding at December 31, 2014. OnJuly 1, 2015 an additional 750,000 shares were issued for cash.Fugate also had stock options outstanding at the beginning and endof 2015 which allow the holders to purchase 225,000 shares ofcommon stock at $20 per share. The average market price of Fugate'scommon stock was $25 during 2015. What is the number of shares thatshould be used in computing diluted earnings per share for the yearended December 31, 2015?

a. 1,695,000

b. 1,455,000

c. 1,331,250

d. 1,320,000