AFM391 Chapter Notes -Aros Research Operating System, Harmonized Sales Tax, Contract

6 Nov 2013

School

Department

Course

Professor

Document Summary

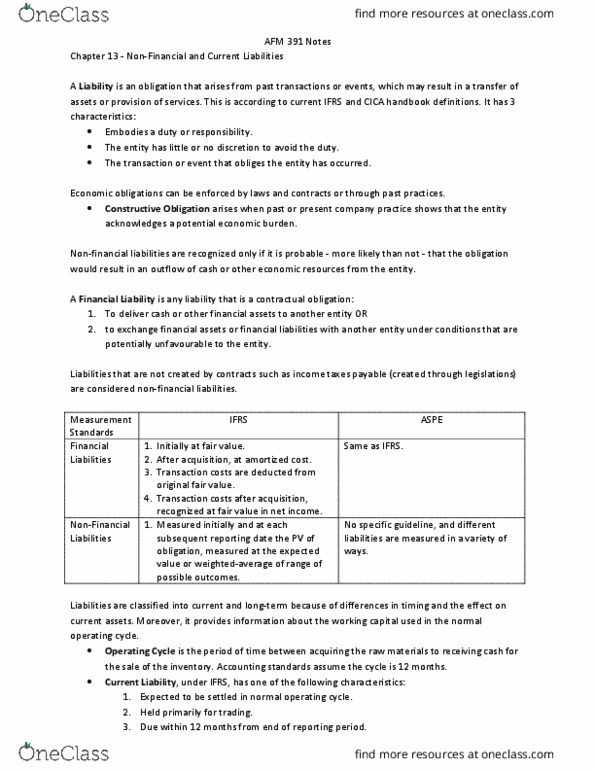

A liability is an obligation that arises from past transactions or events, which may result in a transfer of assets (ifrs) Embody a duty of responsibilities the entity has little or no discretion to avoid the duty the transaction or event that obliges the entity has occurred. A liability of an entity is a present economic obligation for which the entity is the obligor (proposed definition: exist at the present time (balance sheet date) Whether an obligating even has occurred if the event results in a present obligation. How a law or regulation applies to that event: represent economic burdens or obligations. An unconditional promise or other requirement to provide economic resources. Unconditional obligations paying interest not contingent or conditional on a future event. Stand-ready obligation obligor is ready to do whatever is required under the terms of contract. Uncertainty regarding the amount of future outflows of assets. No uncertainty about whether a present obligation exists.