ARBUS102 Chapter Notes - Chapter 3: Historical Cost, Scatter Plot, Contribution Margin

7 Mar 2016

School

Department

Course

Professor

Document Summary

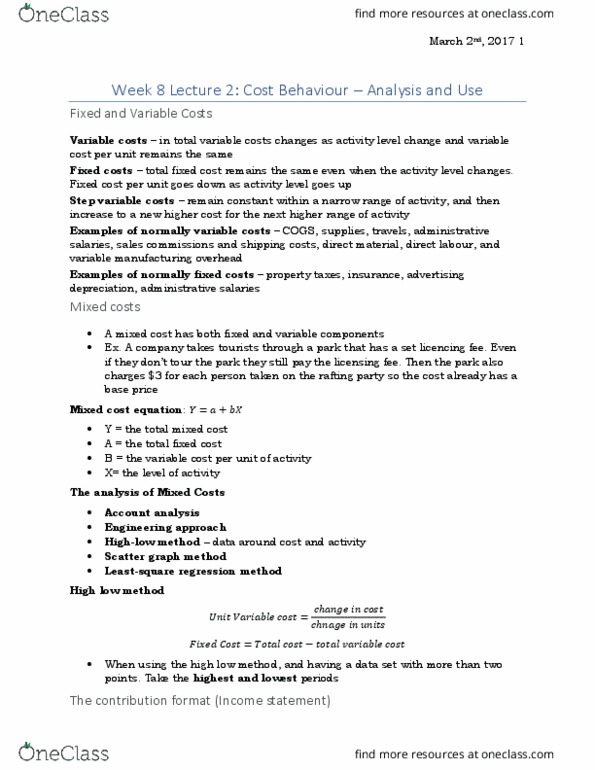

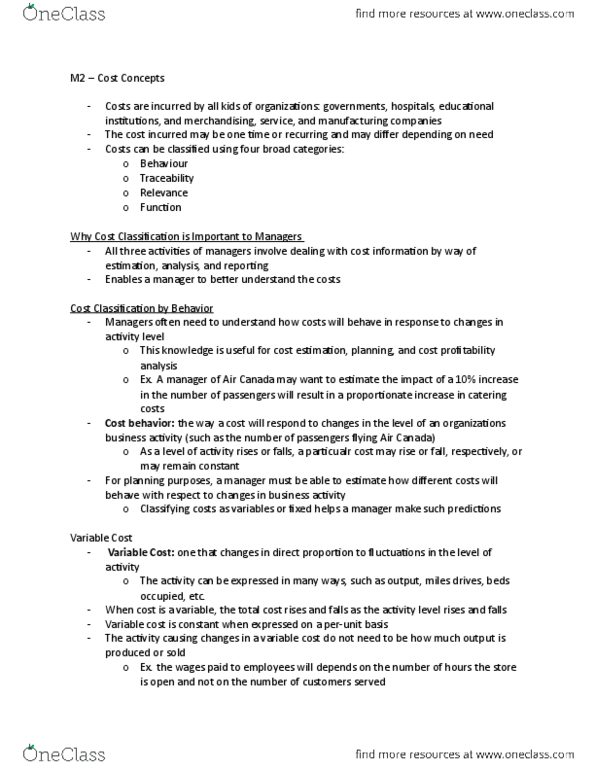

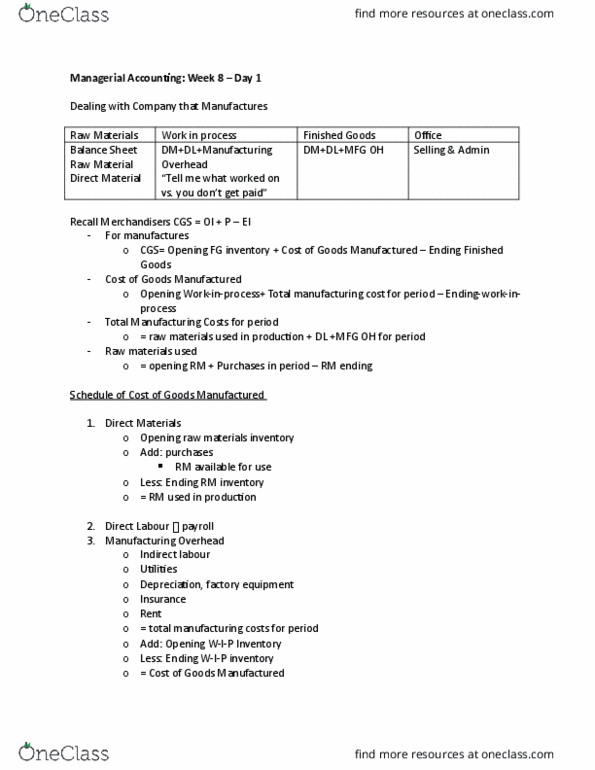

All three cost behaviour patterns variable, fixed, and mixed - are found in most organizations. The relative proportion of each type of cost present in a firm determines its cost structure: a firms cost structure can have a significant impact on decisions. A variable cost remains constant when expressed on a per-unit basis. To plan and control variable costs, a manager must be well acquainted with the various activity bases within the firm. Whether a cost is considered to be variable depends on whether it is caused by the activity under consideration. Most organizations are interested in classifying costs as variable or fixed using an appropriate output-based activity measure as the vase: doing this allows management to make crucial decisions and assess profitability using output as the basis. Some variable costs behave in a true variable or proportionally variable pattern. Other variable costs behave in a step variable pattern.