MTHEL131 Chapter Notes - Chapter 5: Whole Life Insurance, Life Insurance, Term Life Insurance

14 Oct 2013

School

Department

Course

Professor

Document Summary

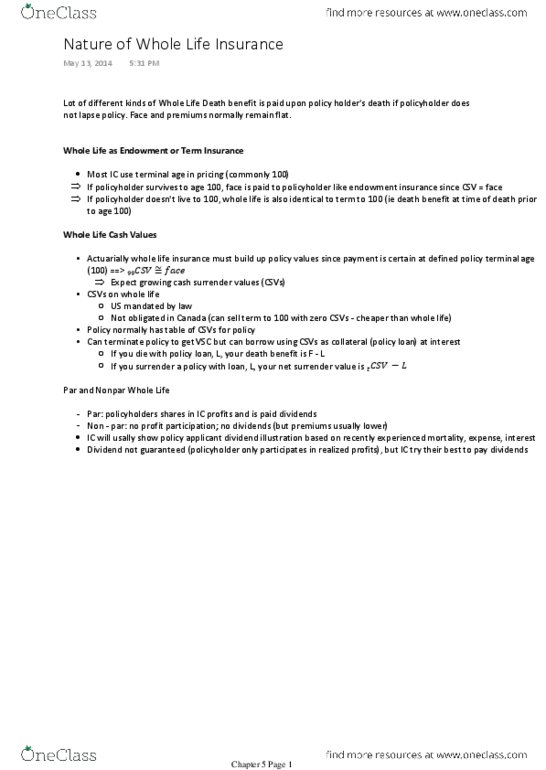

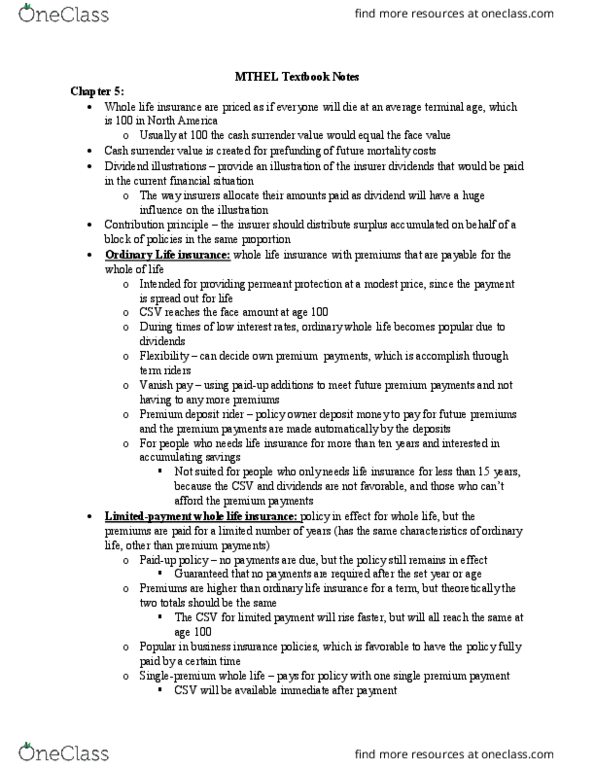

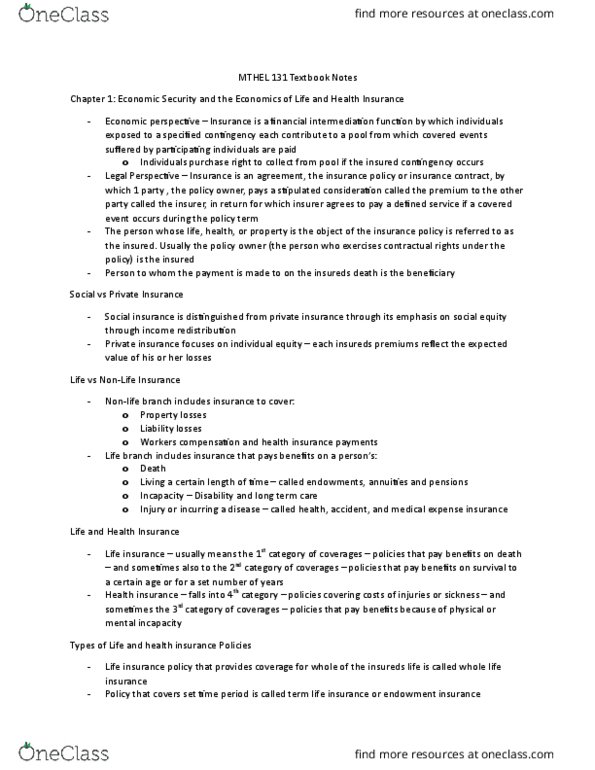

Provides for the payment of the face value upon death, regardless of when the death occurs. Face amount remains the same, but dividends are often used to increase the total benefits paid. Most whole-life insurance is priced based on mortality tables that assume that all insureds die at a certain age (ex. When an insured exceeds that age, insurer pays the policy face amount, as if they had died this is why they"re sometimes referred to as age-100 endowments . Many whole life policies are required to have cash values (which build to policy face amount, usually by age 100) cash values are available to policy-owner at any time they terminate. Under participating policies, dividends may be surrendered for cash, with no influence on the policy. Also, policy owner can obtain a loan up to the policy"s cash value. If not repaid, it is deducted from face value upon death.