MGT426H5 Chapter Notes - Chapter 2: Buyout, Equity Method

Document Summary

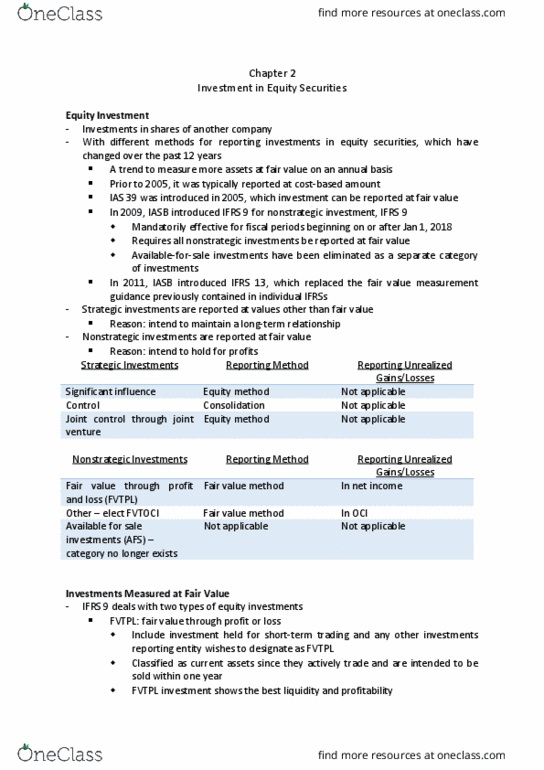

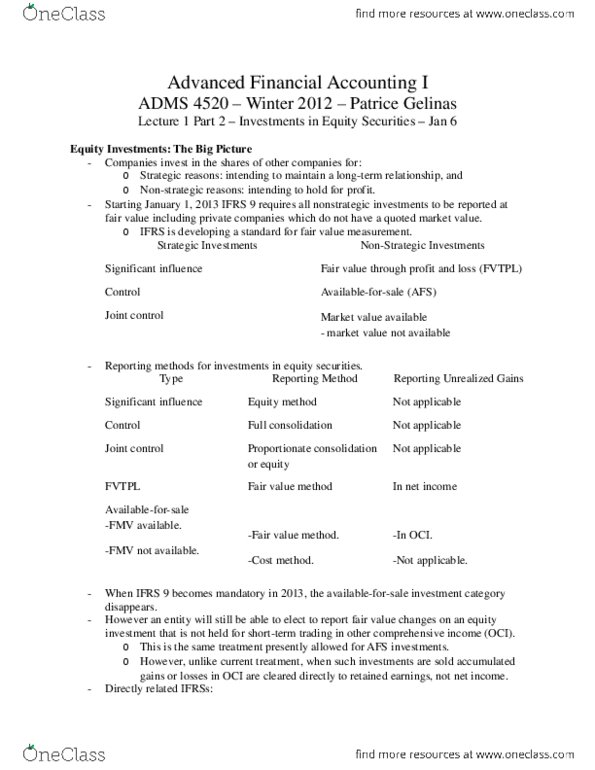

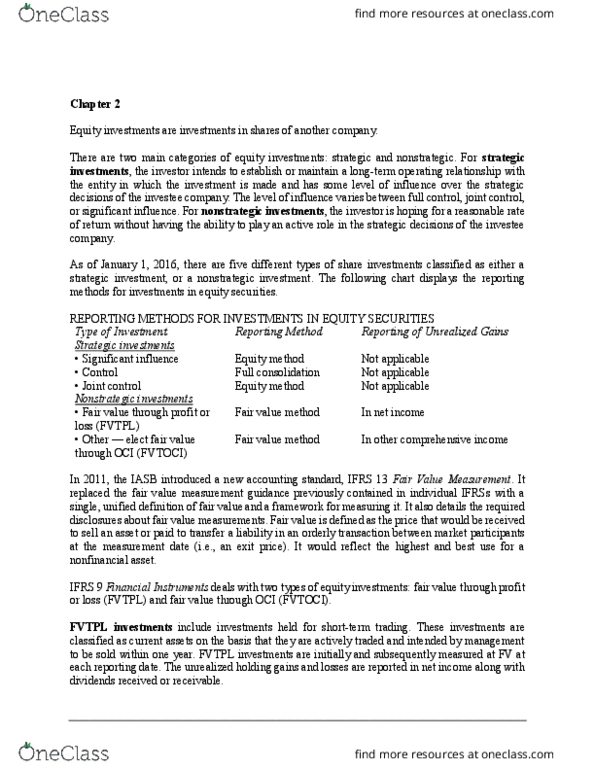

A business combination is a transaction or other event in which an acquirer obtains control of one or more businesses. Transactions sometimes referred to as true mergers" or. Mergers of equals" are also business combinations as that term is used in this ifrs. A parent subsidiary relationship exists when, through an investment in shares or other means, the parent company has control over the subsidiary company. The investee"s equity is increased by income and decreased by dividends. For example, if another shareholder group owned up to 65% of purina"s voting shares, ralston could argue that its ownership did not provide significant influence over purina. In this case, ralston would likely classify the investment as a fvtpl investment and report it at fair value. Alternatively, ralston might argue that its 35% ownership established control over purina. This would occur if, for example, ralston also owned convertible preferred shares that, if converted, would increase its voting share ownership to greater than 50%.