MGT120H5 Chapter Notes - Chapter 4: Canadian Securities Administrators, Internal Control, Smart-1

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

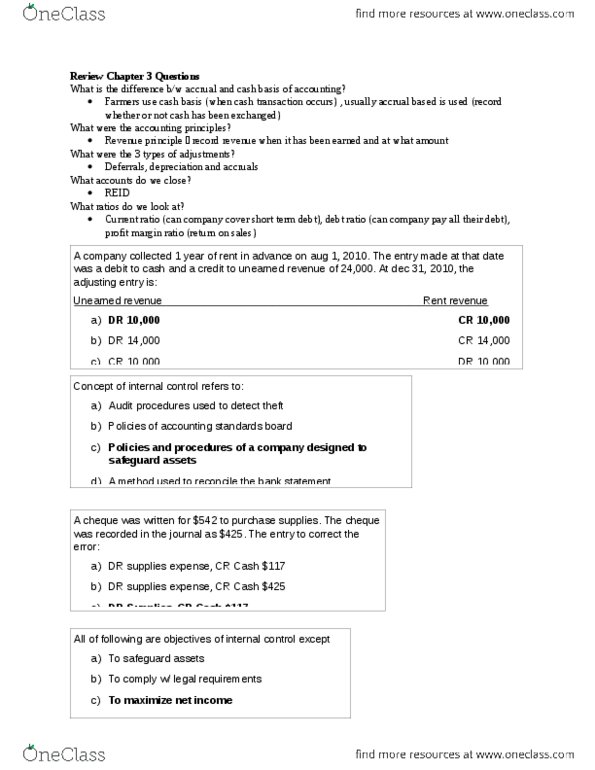

What is the difference between the accrual and the cash basis of accounting. Question #1: a company collected one year of rent in advance on august 1, 2010. The entry made at that date was a debit to cash and a credit to unearned revenue of ,000. At dec. 31, 2010, the adjusting entry is: Unearned revenue rent revenue: debit ,000 credit ,000, debit ,000 credit ,000, credit ,000 debit ,000, credit ,000 debit ,000. Learning objective 1: learn about fraud and how much it costs. Fraud is an intentional misrepresentation of facts, made for the purpose of persuading another party to act in a way that causes injury or damage to that party. It is a huge problem and is getting bigger not only in canada, but across the globe. The two most common types of fraud that impact financial statements are: misappropriation of assets, fraudulent reporting.