MGAB01H3 Chapter : Inventory Basics

27 Oct 2010

School

Department

Course

Professor

16

MGAB01H3 Full Course Notes

Verified Note

16 documents

Document Summary

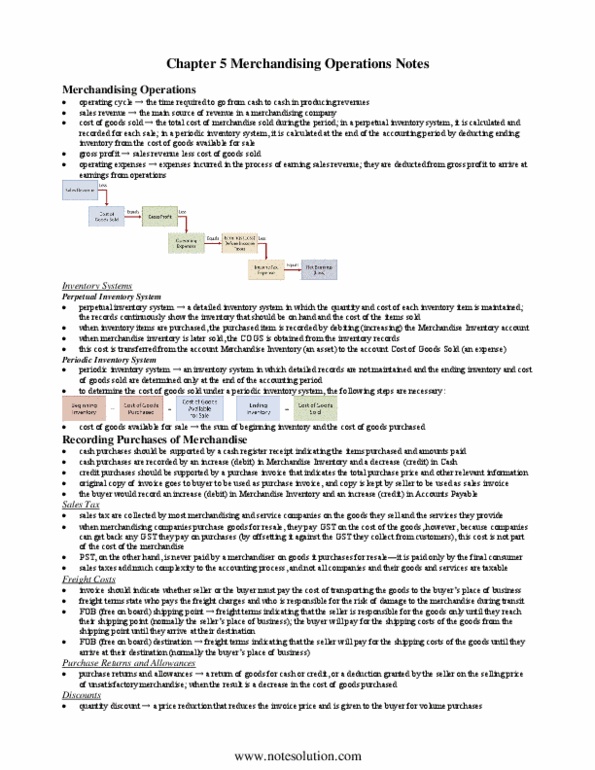

Inventory affects both the balance sheet and the income statement. To determine inventory quantities: (1) take a physical inventory of goods on hand, and (2) determine the ownership of goods. N usually done when business is closed or slow. N units costs are then applied to the quantities in order to determine the total cost of the inventory. N to make sure that inventory quantities truly belong to the company. N goods in transit: the shipping details allow the company to decide if the inventory in transit is their responsibility or the other . 425,308 responsibility. If it is the responsibility is in our company, then the inventory in transit should be taken into consideration. N consigned goods: under a consignment arrangement, the holder of the goods (consignee) does not own the goods. Ownership remains with the shipper of the goods (consignor). Therefore, the goods should not be considered for the consignee and should be considered for the consignor.