MGAB03H3 Chapter Notes - Chapter 2: Sunk Costs, Variable Cost, Decision-Making

22 Oct 2013

School

Department

Course

Professor

Document Summary

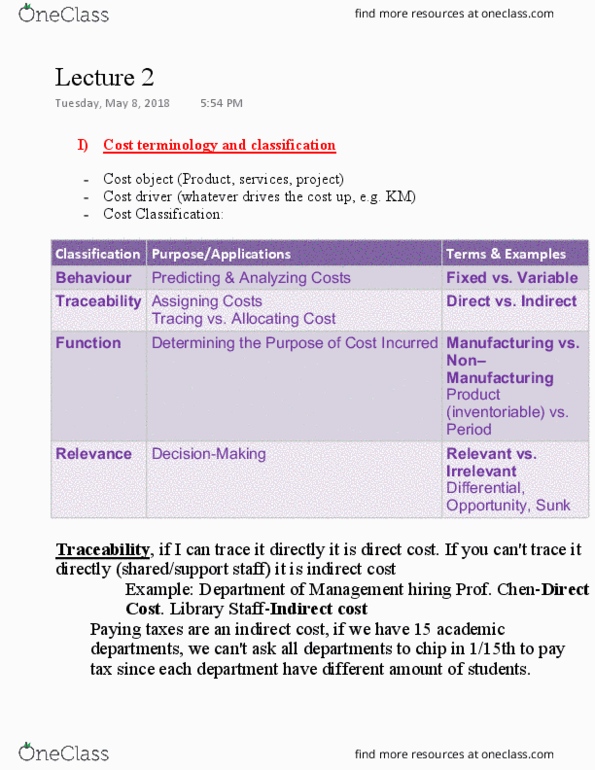

5 categories of cost: relevance, behaviour, traceability, function, controllability. Relevant revenues & costs: r revs & costs that will differentiate btwn alternatives that will occur in the future. Irrelevant revs & costs:will not make a difference to either alternatice they have no bearing on the decision. Sunk costs: irrelevant cost bc the cost has already been incurred & cannot b avoided now. Cost object: a thing r activity for which we measure costs. Diret costs: costs that r directly traced back to a cost object n is incurred for the benefit of a particular object. Indirect costs: incurred for the benefit of more than 1 cost object & cant b easily traced back to a particular cost object. Direct materials & direct labour aka. Direct labour & manufacturing overhead aka. Exhibit 2. 1: cost classifications, applications, and cost terms. Manufacturing cost vs. nonmanufacturing cost (product vs. period)