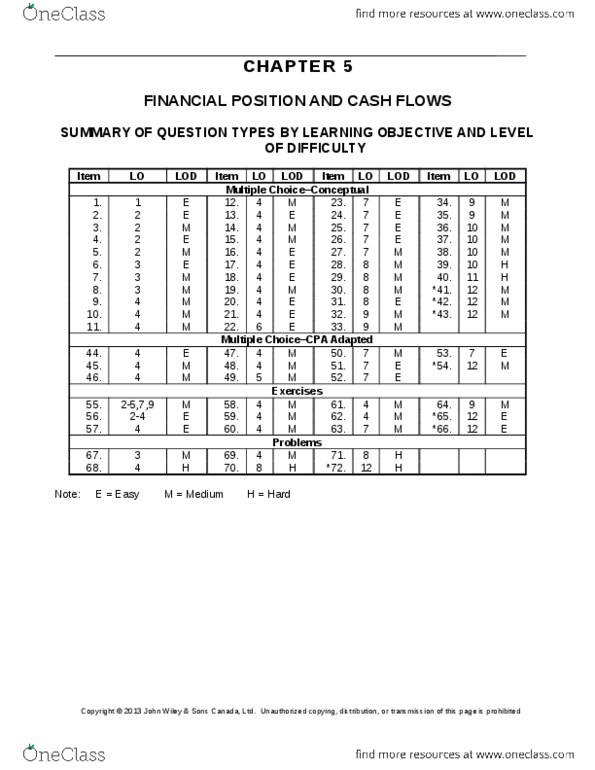

MGAC01H3 Chapter Notes - Chapter 5: Cash Flow, Financial Statement, Historical Cost

Document Summary

Chapter 5 financial position and cash flows notes. Limitations of the balance sheet some of the major limitations of the balance sheet are: many assets and liabilities are stated at their historical cost. As a result, the information that is reported in the balance sheet has higher reliability but it can be criticized as being less relevant than the current fair value would be. Judgments and estimates are used in determining many of the items reported in the balance sheet. 2: the balance sheet necessarily leaves out many items that are of relevance to the business but cannot be recorded objectively. Because liquidity and solvency ratios worsen when liabilities are recognized, a company may be biased against including liabilities in the financial statements. Knowing this, analysts habitually look for and capitalize many liabilities that may be off-balance sheet before they calculate key liquidity and solvency ratios.