MGAC01H3 Chapter Notes - Chapter 2: Income Statement, Comprehensive Income, Conceptual Framework

Document Summary

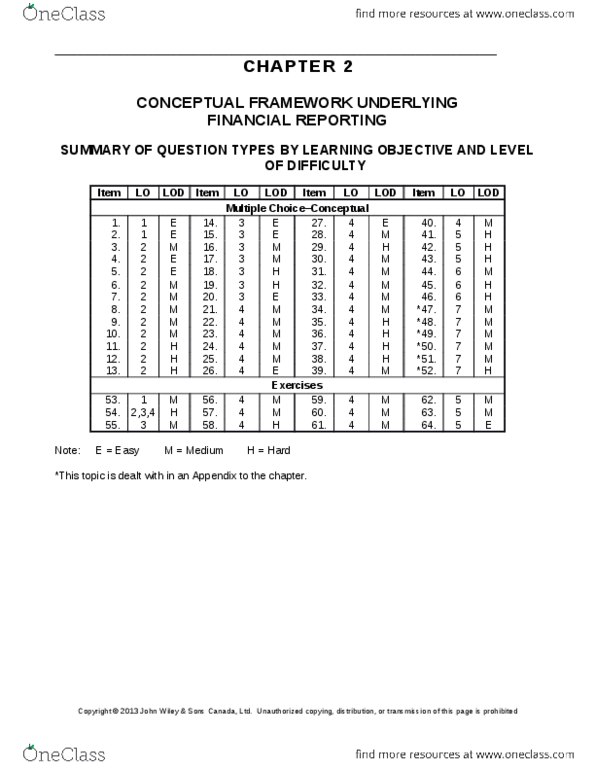

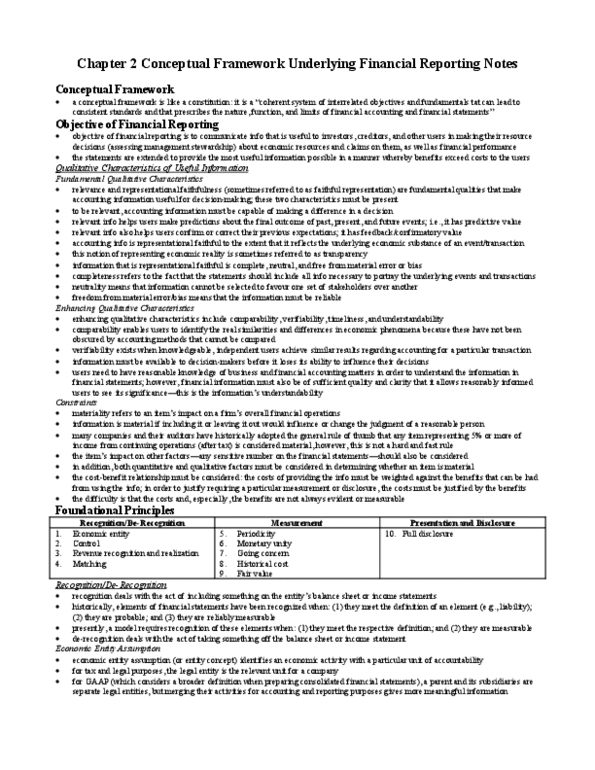

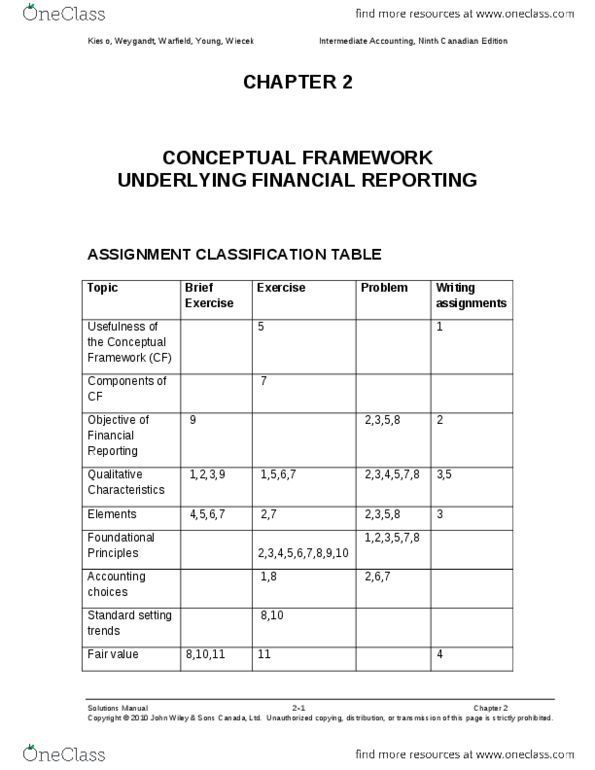

Chapter 2 conceptual framework underlying financial reporting. Describe the usefulness of a conceptual framework. Describe the main components of a conceptual framework for financial reporting. The first level deals with the objective of financial reporting. The second level includes the qualitative characteristics of useful information and elements of financial statements. The third level includes foundational principles and conventions. The objective of financial reporting is to provide information that is useful to individuals making investment and credit decisions. The overriding criterion by which accounting choices can be judged is decision usefulness; that is, the goal is to provide the information that is the most useful for decision-making, fundamental characteristics include relevance and faithful representation. Enhancing characteristics include comparability, verifiability, timeliness, and understandability. Define the basic elements of financial statements. The basic elements of financial statements are (1) assets, (2) liabilities, (3) equity, (4) revenues, (5) expenses, (6) gains, and (7) losses.