MGFB10H3 Chapter Notes - Chapter 7: Weighted Arithmetic Mean, Net Income, Investment

Document Summary

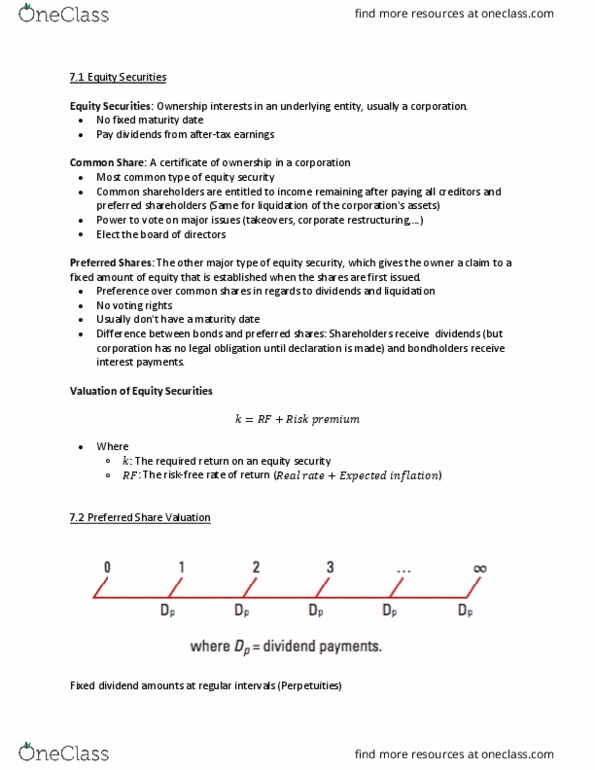

Most preferred shares (ps)have preference over common shares w/ respect to income and assets (in the event of liquidation) but they rarely have any voting rights. We estimate the expected future cash flows associated w/ the security and then determine the discounted present value of those future cash flows based on an appropriate discount rate (k) The discount rate for equities will equal the risk-free rate of return plus a risk premium (like bonds): k= rf + risk premium, k= the required return on an equity security, rf= the risk-free rate of return. Risk-free rate comprises the real rate of return plus expected inflation. Risk premium will be based on an estimate of the risk associated w/ security (higher the risk, higher the premium) Along w/ the discount rate, investors must estimate the size and timing of the expected cash flows associated w/ n equity security. B/c preferred shares dividend payments are indefinite, we can call these investments.