MGEB02H3 Chapter : Week 11 chapter notes

5 Dec 2010

School

Department

Course

Professor

Document Summary

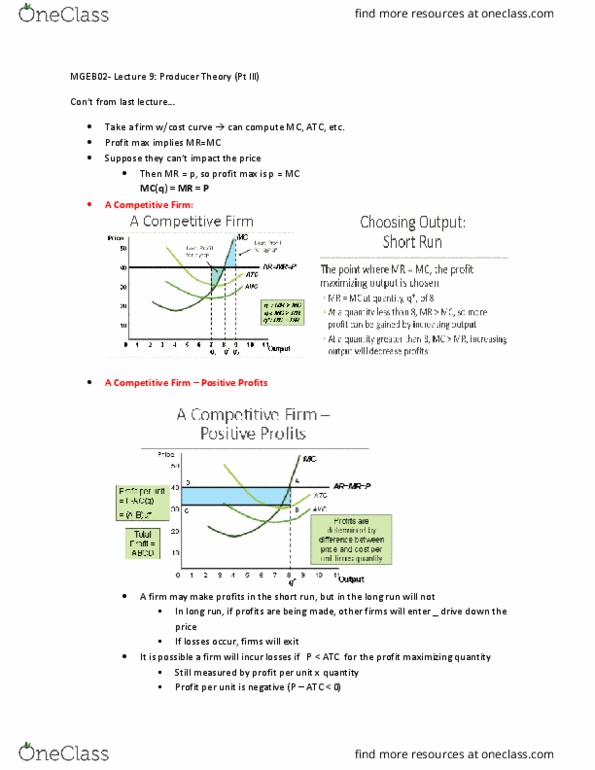

Chapter 8 profit maximization and competitive supply notes. N model of perfect competition rests on 3 basic assumptions: (1) price taking, (2) product homogeneity, and (3) free entry and exit. N when products are heterogeneous, each firm has opportunity to raise its price above its competitors without losing all of its sales. N free entry (or exit) condition under which there are no special costs that make it difficult for firm to enter (or exit) an industry. N as a result, buyers can easily switch from one supplier to another, and suppliers can easily enter or exit a market. N managers then have some leeway in how they run the firm and can deviate from profit-maximizing behaviour. N managers may be more concerned with such goals as revenue maximization, revenue growth, or the payment of dividends. 8. 3 marginal revenue, marginal cost, and profit maximization. N marginal revenue change in revenue resulting from a one-unit increase in output.