MGTA01H3 Chapter Notes - Chapter 1: Demand Curve, Economic Equilibrium, Oligopoly

14

MGTA01H3 Full Course Notes

Verified Note

14 documents

Document Summary

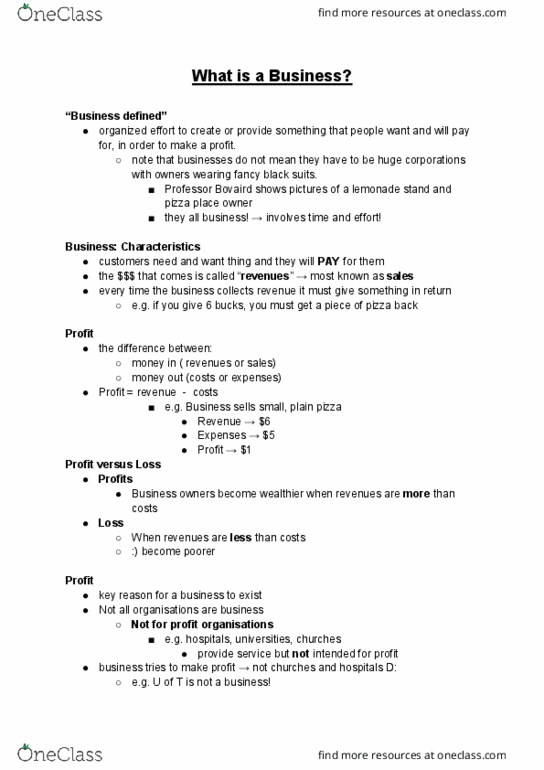

Business: an organised effort, to make or sell something, to sell to customers, who need or want something, in order to make a profit. Customers need and want things and they will pay for them. Profit is what remains after business"s expenses have been subtracted from its revenues. The difference between money in (revenues or sales) and money out (costs or expenses) A business exists to make a profit. Not all organisations are businesses: e. g. hospitals, universities, churches. These do provide services: but not intended for profit. Expenses: the money a business spends producing it"s goods and services and generally running the business (also referred to as costs ). Revenues: the money a business earns selling its products and services. Most profitable companies in 2005 were royal bank of canada (. 3 billion), manulife. Financial (. 2 billion), and imperial oil ltd. (. 6 billion) Businesses must take into account what consumers want or need (demand for it"s goods or services)