MGFC10H3 Chapter 16: Chapter 16 Notes

Document Summary

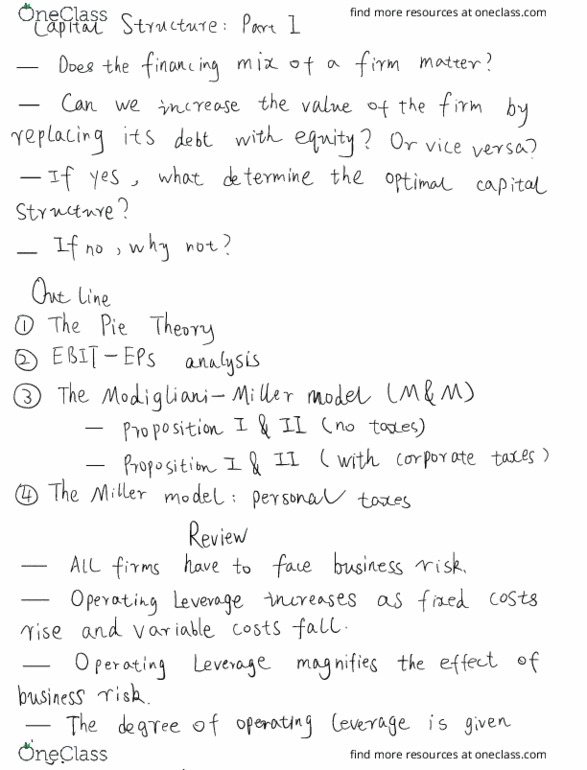

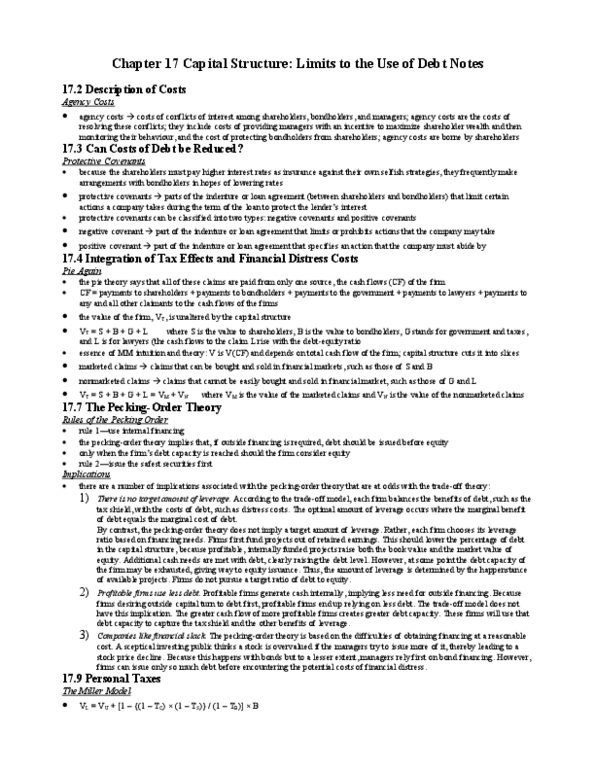

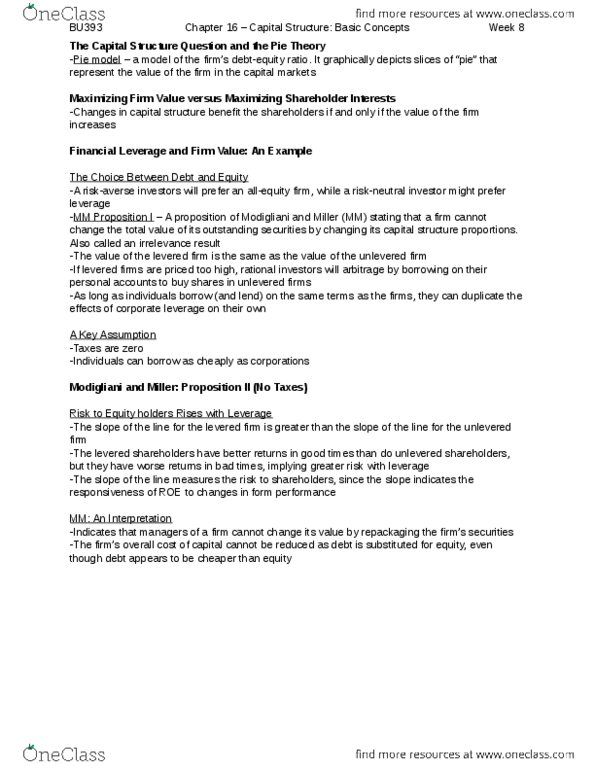

16. 3 financial leverage and firm value: an example. 16. 4 modigliani and miller: proposition ii (no taxes) S = [(ebit rbb) (1 tc)] / rs the numerator is the expected cash flow to levered equity after interest and taxes the denominator is the rate at which the cash flow to equity is discounted. Expected return and leverage under corporate taxes: mm proposition ii (corporate taxes): rs = r0 + (b / s) (1 tc) (r0 rb) The weighted average cost of capital, rwacc, and corporate taxes: vl = [ebit (1 tc)] / rwacc. In a world of no taxes, the famous proposition i of modigliani and miller proves that the value of the firm is unaffected by the debt-to-equity ratio. In other words, a firm"s capital structure is a matter of indifference in that world. The authors obtain their results by showing that either a high or a low corporate ratio of debt to equity can be offset by homemade leverage.