MGFC10H3 Chapter 19: Chapter 19 Notes

Document Summary

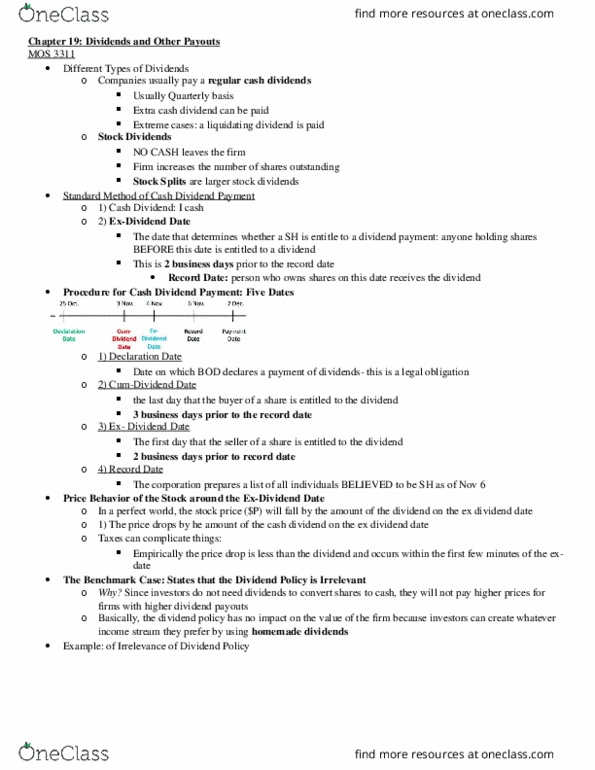

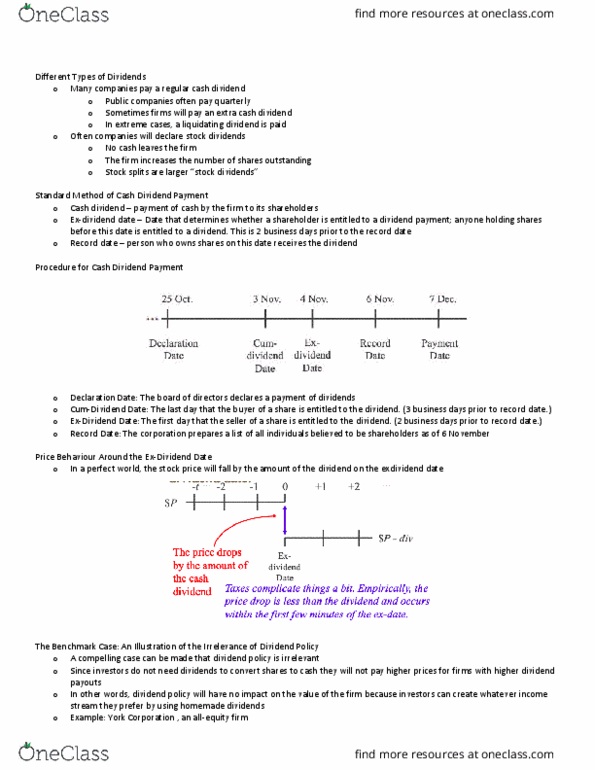

19. 3 the benchmark case: an illustration of the irrelevance of dividend policy. Current policy: dividends set equal to cash flow. The indifference proposition: mm makes the following assumptions: the npv of the firm can be calculated by discounting these dividends the firm"s value can be expressed as. V0 = div0 + (div1 / 1 + rs: there are neither taxes nor brokerage fees, and no single participant can affect the market price of the security through his or her trades. 5 reasons why firms choose repurchases over dividends are: flexibility. It is well known that firms view dividends as a commitment to their shareholders and are quite hesitant to reduce an existing dividend. Thus, a firm with a permanent increase in cash flow is likely to increase its dividend. Conversely, a firm whose cash flow increase is only temporary is likely to repurchase shares of stock: executive compensation. Executives are frequently given stock options as part of their overall compensation.