RSM100Y1 Chapter Notes - Chapter 16: Canada Deposit Insurance Corporation, Nasdaq, Electronic Funds Transfer

Document Summary

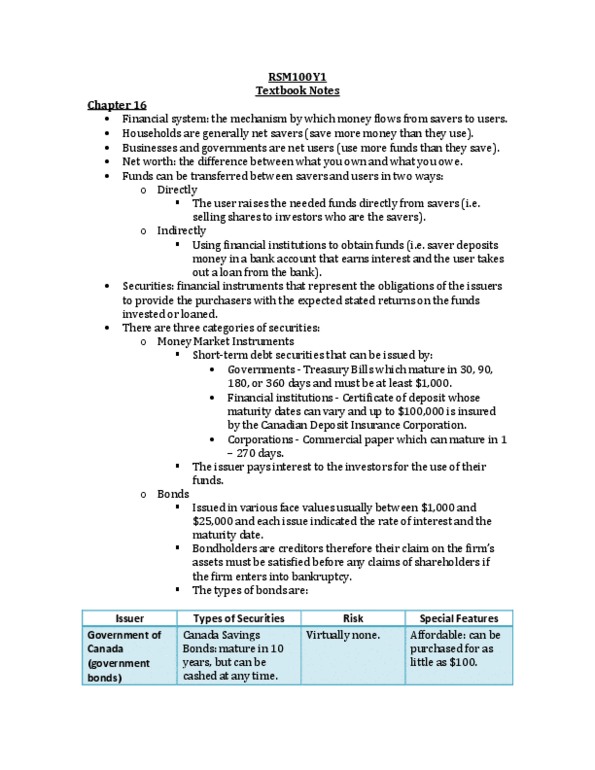

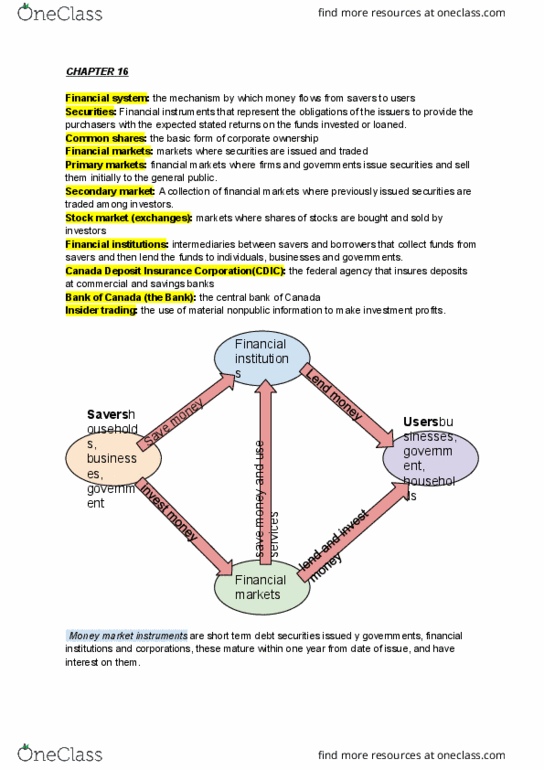

As people age, they often move form being net borrows to being net savers. Funds can be transferred between savers and users in two ways: directly and indirectly. A direct transfer means that the user raises the needed funds directly from savers. (do occur, but most funds flow through financial markets or financial institutions. ) Securities, also called financial instruments, represent the obligations of the issuers- businesses and governments- to provide the purchaser with the expected or stated returns on the funds invested or loaned. Three categories: money market instruments, bonds, and shares (also known as stock) Money market instrument and bonds are debt securities. Shares are units of ownership in public corporations. Money market instruments are short-term debt securities issued by governments, financial institutions, and corporations. All money market instruments mature within one year from the date of issue. They are generally low-risk securities and are purchased by investors when they have surplus cash.