RSM222H1 Chapter Notes - Chapter 7: Activity-Based Costing, E.G. Time, Product Design

Document Summary

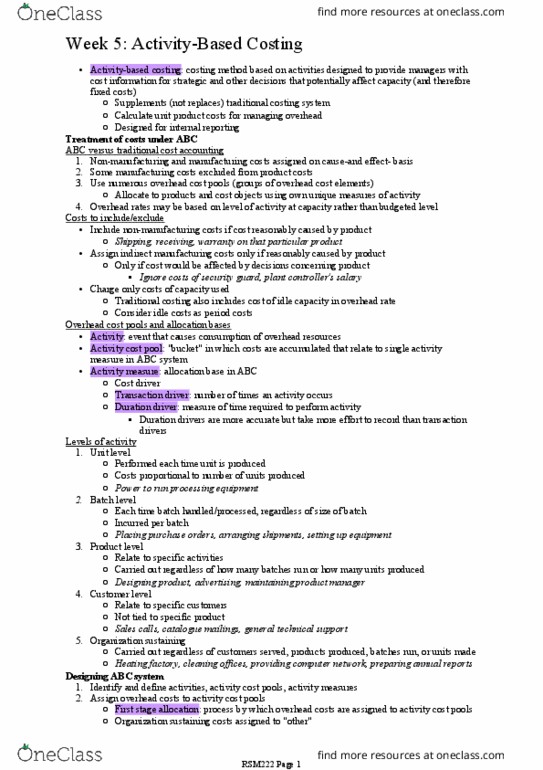

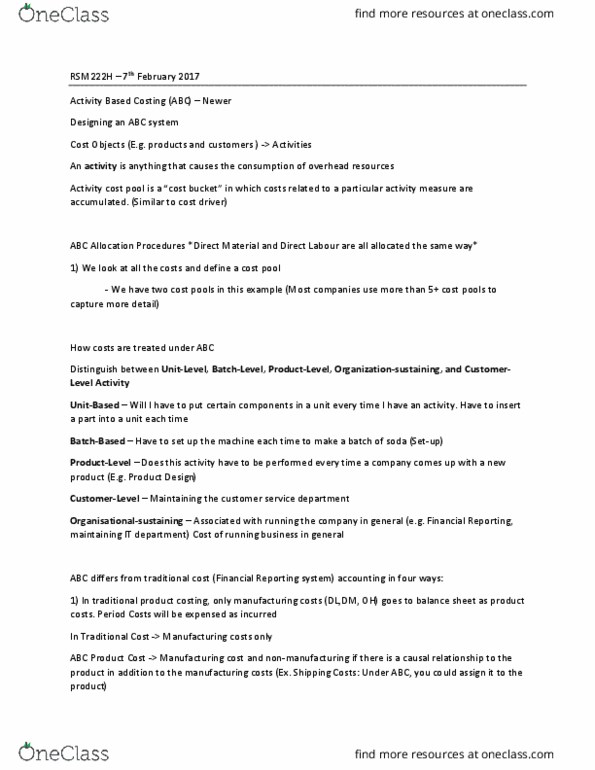

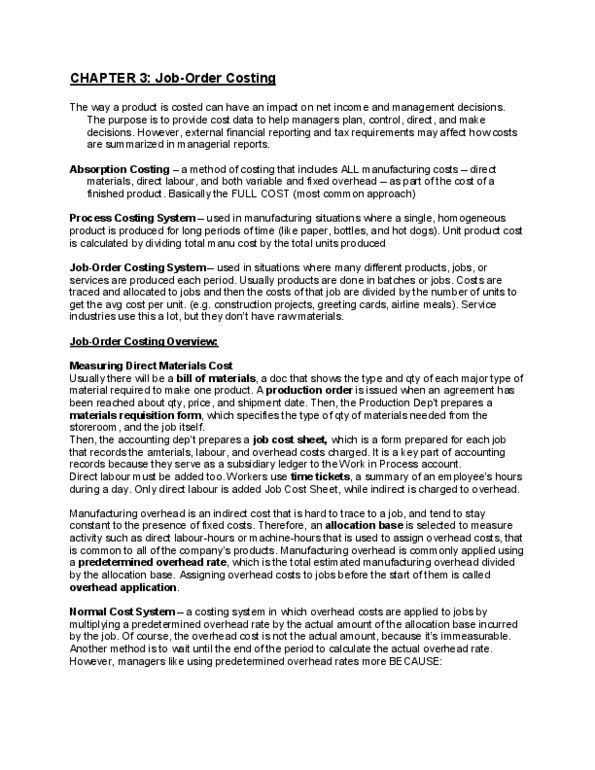

Designed to provide managers w cost information to help make decisions affecting capacity hence fixed costs and variable costs. Overhead refers to indirect manufacturing costs and non-manufacturing costs in abc. Manufacturing costs that don"t directly affect the product excluded in product cost. A bucket in which costs are accumulated that relate to one activity measure in the abc system. Also called a cost driver: transaction drivers, duration drivers. Simple count of the # of times an activity occurs. Measure of the amount of time required to perform an activity. For e. g. time spent on each order: unit level activities, batch-level activities, product-level activities, customer-level activities, organization-level activities. Cost based on # of batches processed or handled. Or cost based on # of customer orders (number of units inside each batch is irrelevant) Activities carried out regardless of whether product is sold. For e. g. designing product, advertising, maintaining product management staff etc. Cost based solely on activities for that customer.