RSM220H1 Chapter Notes - Chapter 1: Financial Statement, Moral Hazard, Adverse Selection

Document Summary

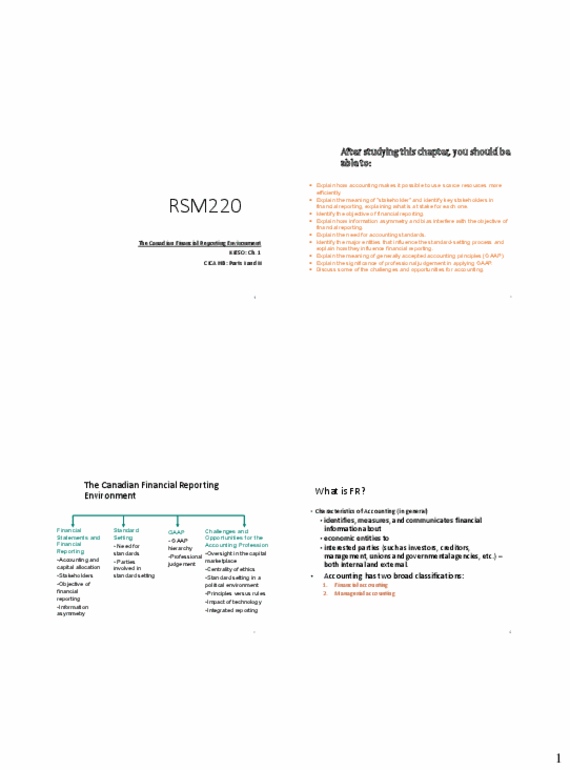

Week 1: chapter 1: the canadian financial reporting. 1: about economic entities, to interested persons. Accounting and capital allocation: accounting measures company performance accurately and fairly on timely basis. Objective of financial reporting: provide financial information about reporting entity that is useful to present and potential investors in making decisions in their capacity as capital providers. Decision-usefulness approach: should also adopt entity perspective. Companies viewed as separate and distinct from owners. Proprietary prospective (financial reporting focusing only on needs on shareholders) is not appropriate: investors want to assess, ability to generate net cash inflow, management"s ability to protect and enhance investments. Financial reporting should help identify amount, timing, and uncertainty of cash inflows. Dividends or interest, proceeds from sale, redemption/maturity of securities and laons. Information asymmetry: management may feel too much disclosure hurts competitive advantage, capital markets are inefficient, human behaviour. Not all information is incorporated into stock price. Management shares only positive info to maximize personal bonus.