🏷️ LIMITED TIME OFFER: GET 20% OFF GRADE+ YEARLY SUBSCRIPTION →

Pricing

Log in

Sign up

Home

Homework Help

Study Guides

Class Notes

Textbook Notes

Textbook Solutions

Booster Classes

Blog

Home

Textbook Notes

300,000

CA

170,000

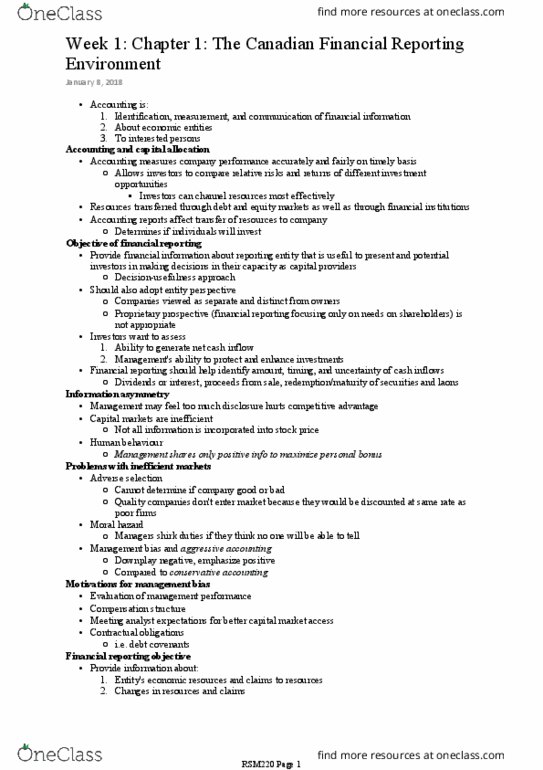

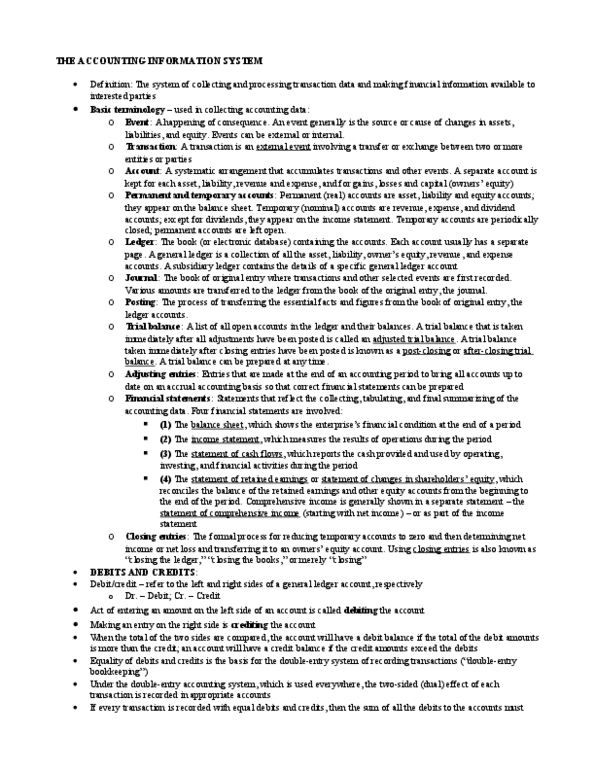

RSM220H1 Chapter 1: CHAPTER 1 TEXTBOOK REVIEW A six page summary of the entire first chapter of the RSM220 Textbook (Intermediate Accounting)

60

views

6

pages

orchidporcupine823

16 Oct 2011

School

UTSG

Department

Rotman Commerce

Course

RSM220H1

Professor

Dragan Stojanovic

2

For unlimited access to Textbook Notes, a

Class+

subscription is required.

Get access

Yearly

Monthly

Yearly

Grade+

20% off

$8

USD/m

$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8

USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Continue

Related Documents

RSM220H1 Chapter Notes - Chapter 1: Financial Statement, Moral Hazard, Adverse Selection

lilacoyster158

RSM220H1 Lecture : CHAPTER 3 TEXTBOOK REVIEW A 6 page summary of the entire third chapter of the RSM220 textbook (Intermediate Accounting)

orchidporcupine823

RSM220H1

Final Exam

Study Guide

RSM220H1 Midterm: RSM220-14S - Midterm - marking guideline (for posting).pdf

blushelk273