RSM321H1 Chapter Notes - Chapter 8: Cash Flow Statement, Equity Method, Cash Flow

Document Summary

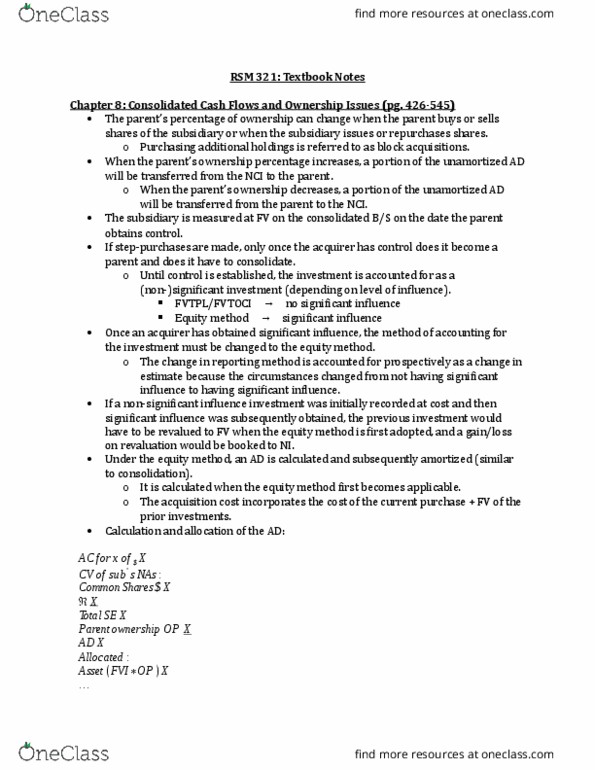

While this statement could be prepared by combining the separate cash flow statements of the parent and its subsidiaries, this would involve eliminating all intercompany transactions, including intercompany transfers of cash. It is much easier to prepare the cash flow statement using comparative consolidated balance sheets and the consolidated income statement, because these statements do not contain any intercompany transactions. The next topic was concerned with changes in the parent"s percentage ownership and the effect that such changes have on the non-controlling interest and particularly on unamortized acquisition differentials. These ownership changes also require special attention when the consolidated cash flow statement is prepared. The parent"s percentage of ownership can change when the parent buys or sells shares of the subsidiary or when the subsidiary issues or repurchases shares. Any time the parent"s percentage of ownership increases, we will account for the transaction as a purchase.