RSM324H1 Chapter 10: Individuals: Determination of taxable income and taxes payable

Document Summary

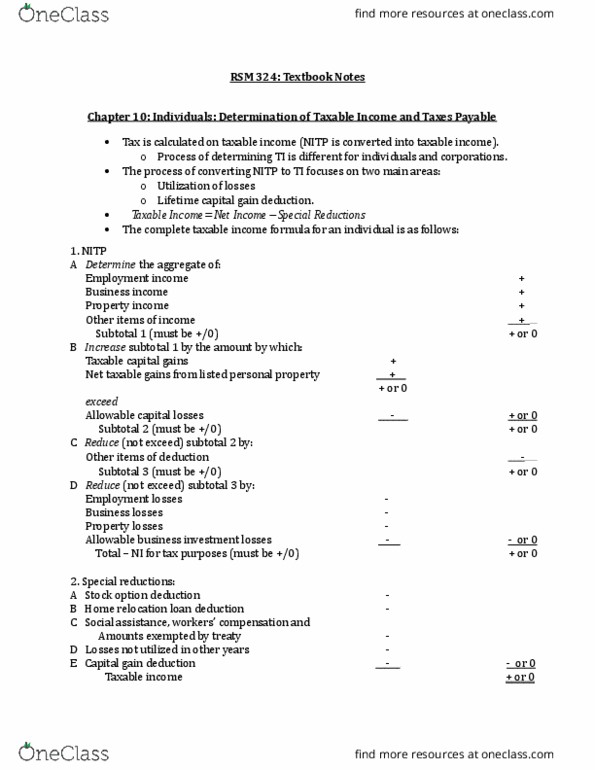

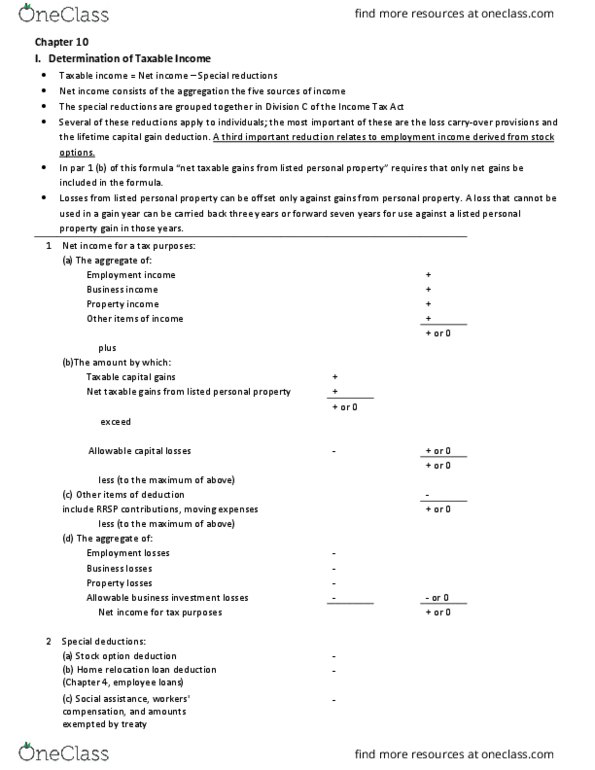

Taxable income = net income division c deductions. Losses incurred in a particular taxation year can be offset against other sources of income, provided they follow the restrictions. Capital losses can be deducted only to the extent that capital gains were realized in the year. Losses from business, employment, and property, and allowable business investment losses, can be offset against all other sources of income. Loss carry-overs are deducted as special reductions after the taxpayer has determined net income for that particular year. Losses incurred in the particular year must be deducted first, as part of net income, before losses of other years can be applied. Allowable capital losses incurred in a current year, if they cannot be utilized in arriving at. These can be carried back three years and forward indefinitely. During this carry-over period, the net capital losses can be deducted only to the extent that the taxpayer has realized net capital gains.