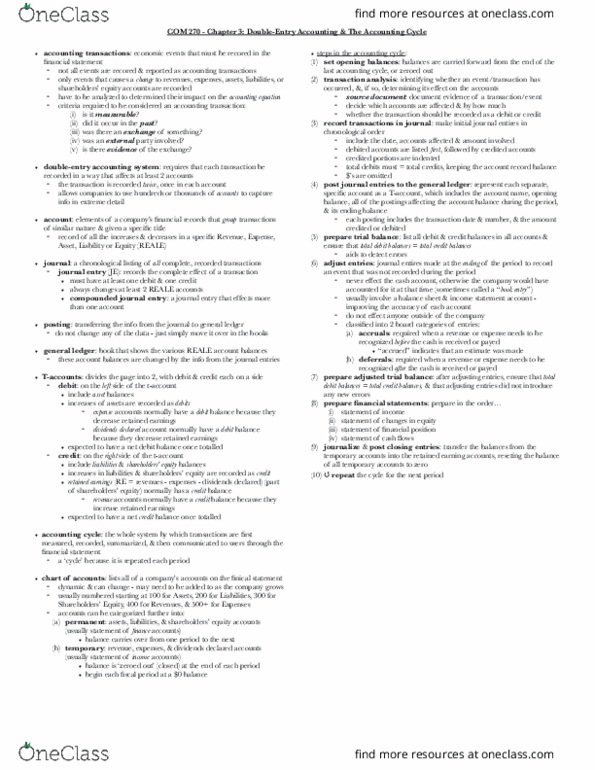

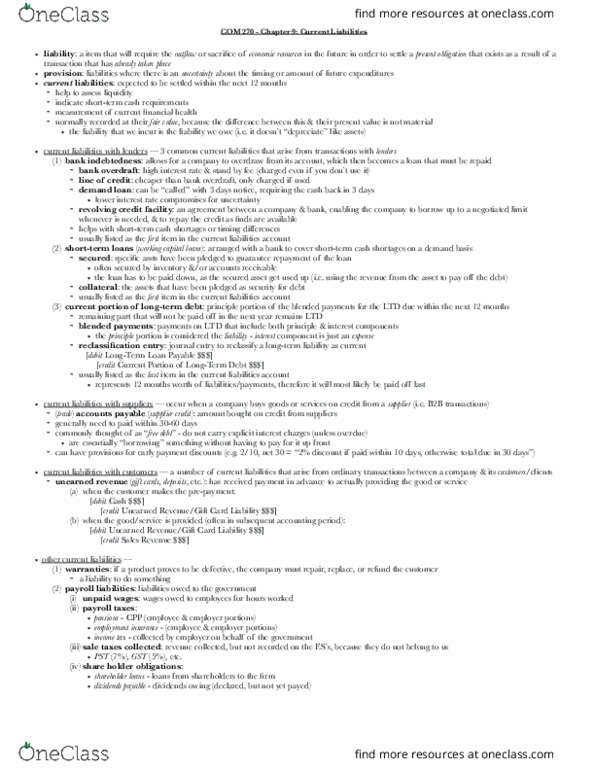

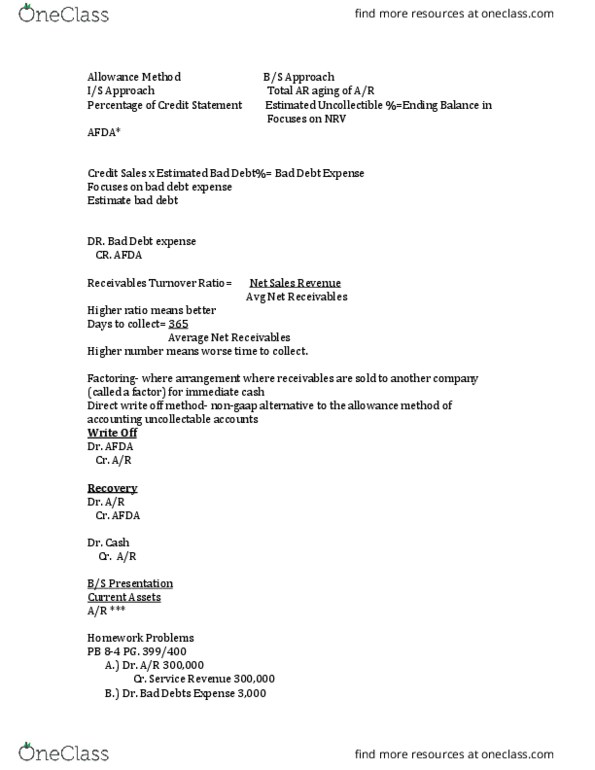

COM 270 Chapter Notes - Chapter 6: Market Liquidity, Subledger, Debits And Credits

29 Jan 2017

School

Department

Course

Professor

Document Summary

Com 270 - chapter 6: cash & accounts receivable: cash: a company"s most liquid asset provides the resources necessary to meet their immediate, short-term. Nancial obligations includes physical cash on hand, amount in bank accounts, & customers" cheques held for deposit cash equivalents: can easily be converted into known amounts of cash, & matures in 90 days or less (ex. government treasury bills) Re ected in statement of nancial position at their carrying amount carrying amount = gross accounts receivable - allowance doubtful accounts. Allowance for doubtful accounts (afda) (allowance for credit losses): a contra account to account receivables, re ecting the estimated amount of accounts receivable that will not be collected: uses the allowance method. 3 key transactions that may occur under the allowance method: (2) establishing allowance & recording bad debt expenses: recorded in the contra-asset account, allowances for.