ACCT 1510 Chapter Notes - Chapter 2: General Ledger, Faithful Representation, Trial Balance

20 Jun 2018

School

Department

Course

Professor

CHAPTER 2 – The Accounting Information System

Accounting cycle – pocess of transforming results of company’s activities into financial

statements:

1. Analyse transactions

2. Journal Entries

3. Posting (recording) to general ledger

4. Prepare unadjusted trial balance

5. Adjusting journal entries

6. Adjusted trial balance

7. Prepare Financial statement

8. Close books (general ledger) for year

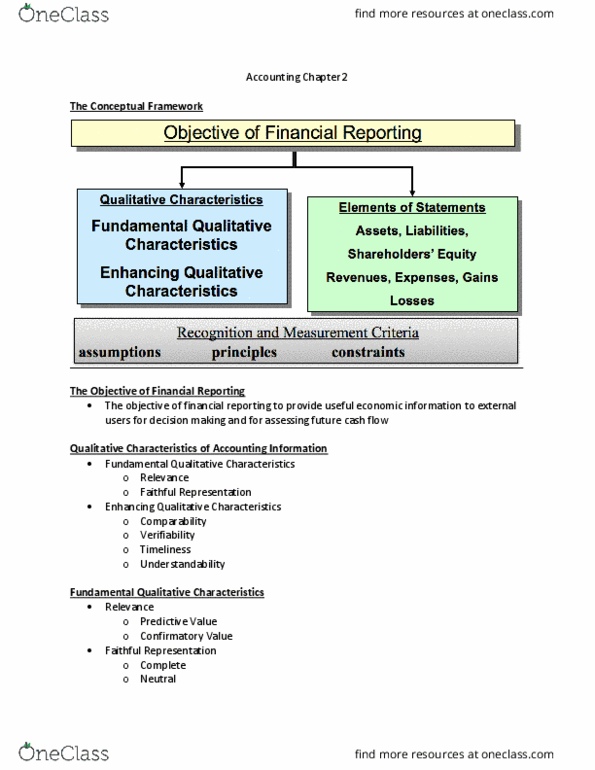

Conceptual Framework

Fundamental objective of financial reporting – provide information that is useful in making

business decisions

a. Qualitative Characteristics (relevance and faithful representation are most important)

- Relevance – information is relevant is it affects a decision

- Predictive value – used to predict future

- Feedback value – what happened in the past

- Information is material – if omission or misstatement of information could

influence a decision

- Faithful representation – information presented represents economic events

unbiasly (neutral), free from error (accurately) and complete

- Comparability – when information can be compared to other similar information

- Consistency – same accounting rules used in previous term as current period

- Verifiability – an independent person would het the same numbers as the company

did (documentation to support the data)

- Timeliness – information is needed to quickly respond to changes/problems

occurring, information should be available before it loses its ability to influence

decisions

- Understandibility – someone with reasonable amount of accounting knowledge can

understand the information

b. Assumptions

- Separate entity – each company is accounted for separate from the owner(s), data

reported separately

- Continuity (Going Concern) – assumption that business can continue on a fulfil its

commitments (for at least a year after financial statement is released)

- Periodicity – life of company is divided into time periods so that income/loss can be

reported more frequently and accurately (monthly, quarterly, annually). Important for

shareholders, owners etc. to know how investment/shares/company is doing.

- Unit of measure – constant purchasing unit (ex. CAD), assumption that the dollar

has same purchasing power throughout the period. (Nonmonetary items (brand

loyalty, customer satisfaction) are therefore not reported since they can’t be

quantified)

Document Summary

Fundamental objective of financial reporting provide information that is useful in making business decisions: qualitative characteristics (relevance and faithful representation are most important) Relevance information is relevant is it affects a decision. Predictive value used to predict future. Feedback value what happened in the past. Information is material if omission or misstatement of information could influence a decision. Faithful representation information presented represents economic events unbiasly (neutral), free from error (accurately) and complete. Comparability when information can be compared to other similar information. Consistency same accounting rules used in previous term as current period. Verifiability an independent person would het the same numbers as the company did (documentation to support the data) Timeliness information is needed to quickly respond to changes/problems occurring, information should be available before it loses its ability to influence decisions. Understandibility someone with reasonable amount of accounting knowledge can understand the information: assumptions.