ACCT 2520 Chapter Notes - Chapter 16: Financial Instrument, Underlying, Market Liquidity

26 Mar 2017

School

Department

Course

Professor

Document Summary

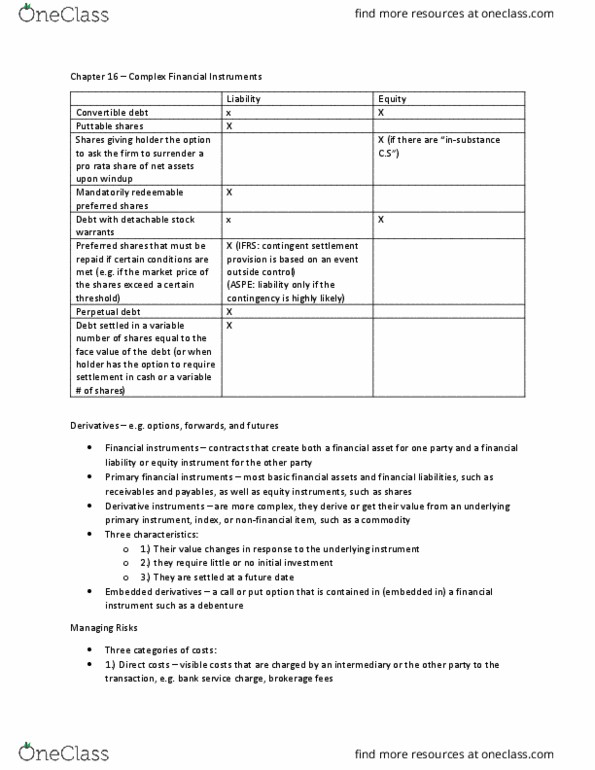

Financial instruments contracts that create both a financial asset for one party and a financial liability/equity instrument for the other party. Primary financial instruments include most basic financial assets/liabilities such as receivables and payables, and equity instruments such as shares. Financial instruments that create rights and obligations that transfer financial risk from one party to the other party. Characteristics: value changes in response to the underlying instrument, require little/no initial investment, settled at a future date. Example: stock options: stock is the underlying , if share price increases, option is worth more, if share price decreases, option may become worthless. Used by: producers and consumers lock in future revenues or costs, speculators and arbitrageurs generate cash profit from trading, maintain market liquidity. Additional motivations to use derivatives: manage interest rate volatility, manage foreign exchange rate volatility. Under ifrs: not accounted for as derivatives, and recognized when goods received if: