Business Administration 2257 Chapter Notes - Chapter 5.2: Gross Margin, Profit Margin, Income Statement

9 Jan 2018

School

Department

Professor

Document Summary

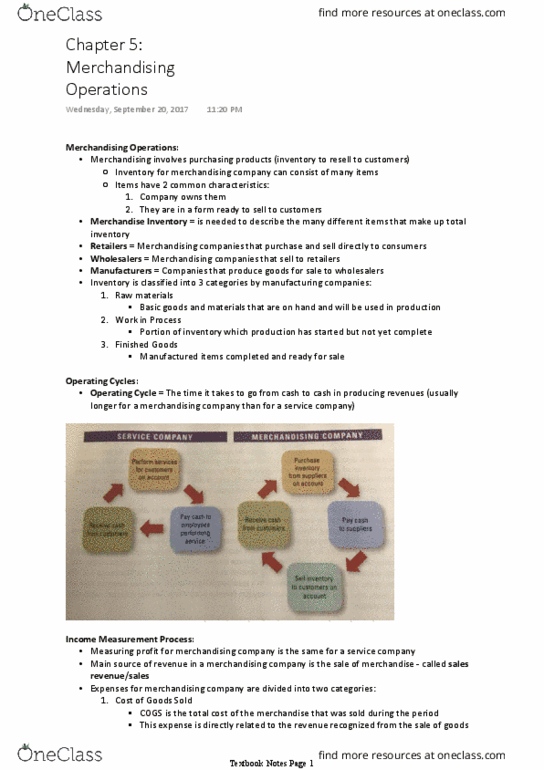

Merchandising companies that purchase and sell directly to consumers are retailers. Merchandising companies that sell to retailers are wholesalers. Merchandising companies that produce goods to sell to wholesalers are manufacturers. Merchandise inventory is already done and in the same state that will be sold to the end customer. Profit in a merchandising company still is revenues expenses. The main form of revenue is sales revenue. Expenses for merchandising companies is divided into two categories: cost of goods sold, the total cost of merchandise sold during the period. In perpetual inventory system, calculated and recorded for each sale. In periodic inventory system, calculated at the end of the accounting period: operating expenses. Beginning inventory plus the cost of goods purchased = cost of goods available for sale. As goods are sold, they are assigned to cost of goods sold. Perpetual inventory system: a detailed inventory system in which the quantity and cost of each inventory item is maintained.