Business Administration 2257 Chapter Notes - Chapter 5: Cash Register, Income Statement, Finished Good

26 Oct 2015

School

Department

Professor

Document Summary

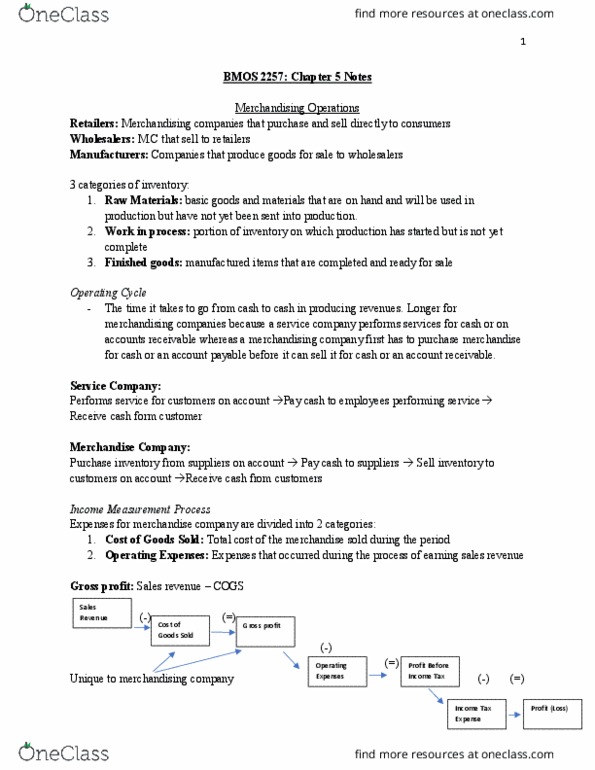

Raw materials: basic goods and materials on hand that"ll be used in production but haven"t been sent into production. Work in process: portion of inventory on which production started but isn"t complete. Finished goods: manufactured items completed and ready for sale. Operating cycle: time it takes to go from cash to cash in producing revenues. In merchandising company, main source of revenue is from sale of merchandise. Sales: expenses for merchandising company divided into 2 categories, cost of goods sold (cogs): total cost of merchandise sold during. Gross profit=sales revenue cogs: operating expense: expenses incurred in process of earning sales period revenue. Cost of goods available for sal e=beginning inventory+cost of goods purchased: ending inventory reported as merchandise inventory asset, cogs reported as cogs expense on income statement. Perpetual inventory system: detailed records maintained for cost of each product that"s purchased and sold.