Business Administration 2257 Chapter Notes - Chapter 3: Accounts Payable, General Ledger, Trial Balance

1 Dec 2012

School

Department

Professor

Document Summary

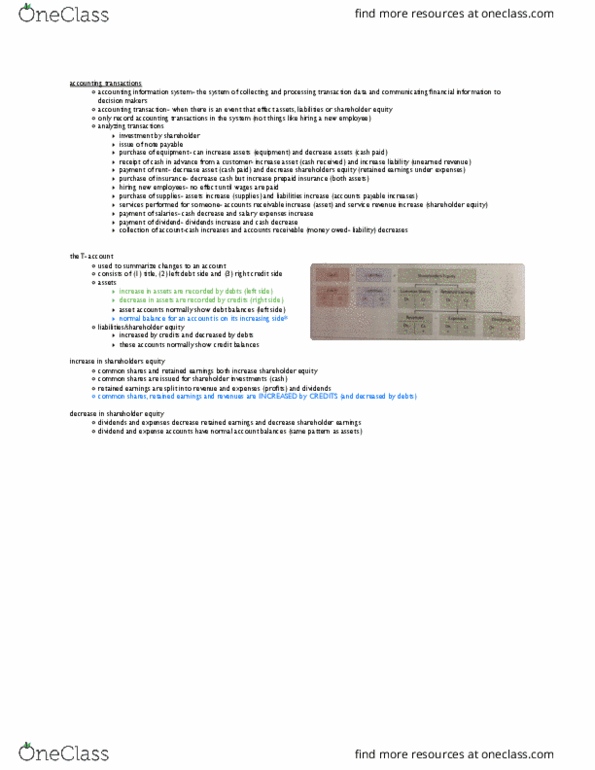

Identify economic event prepare journal entry post entry to g/l (general ledger) . Prep & post adjusting entries prep trial balance prep f/s prep and post closing entries. Cash sales asset and owners" equity increase (cash is an asset and everything has to balance cash carries over to retained earnings which is part of oe) Cash/accounts receivable no impact cash is an asset, so assets go up, but accounts receivable is an asset as well and it"s being reduces because the amount is being paid. Equipment/cash no impact cash is an asset and so is equipment, so when we purchase with cash, cash decreased and equipment increases. It doesn"t impact the equation on a whole. Advertising bill assume you got an invoice from the company and put it in as an accounts payable you decrease both cash and accounts payable. Or you get the bill, decrease your cash with decreases your net income. Dividends paid decrease cash and owners" equity.