Business Administration 2257 Chapter Notes - Chapter 2: Accounts Payable, Deferral, Promissory Note

30 Dec 2013

School

Department

Professor

Document Summary

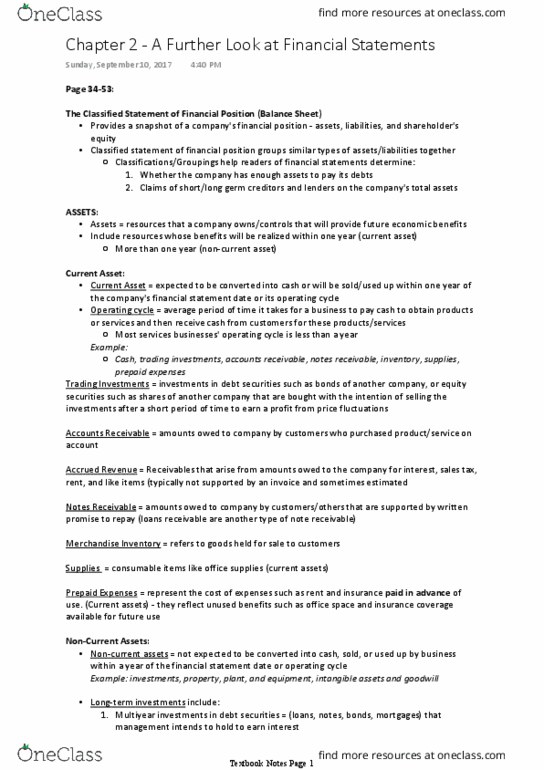

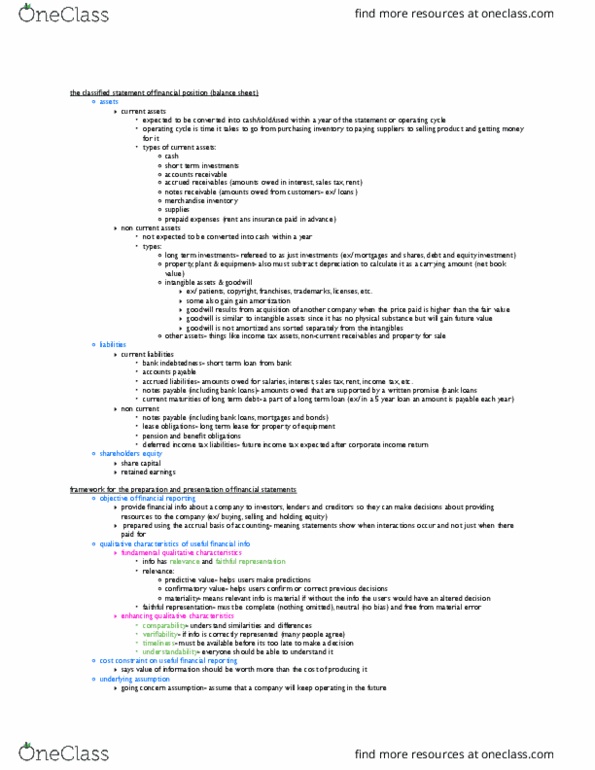

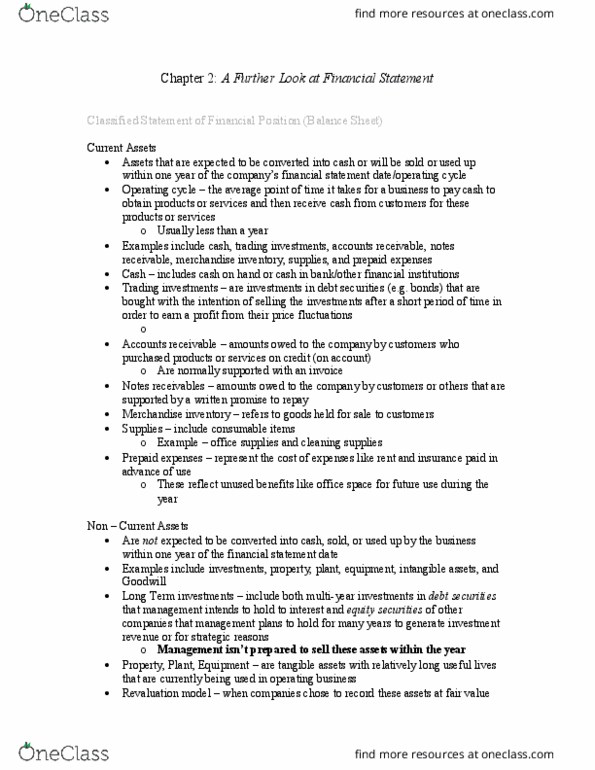

Chapter 2: a further look at financial statements. Current assets assets that can be turned into cash within a year (listed in order of liquidity) Operating cycle the average time it takes to go from cash to cash in producing revenue. Common types of current assets: cash, short-term investments, accounts receivable, accrued receivables, notes receivable, merchandise inventor, supplies, prepaid expenses. Account receivable amounts owed to the company by its customers. Accrued receivable amounts owed to the company for interest, sales tax, rent, and like items. Notes receivable amounts owed to the company by customers that are supported by a written promise to repay. **inventory is a current asset because it will be sold and converted into cash or accounts receivable during the year. **supplies are a current asset because we expect things to be used up by the business within the year. **prepaid expenses are a current asset because they reflect unused benefits available for use during the year.