Management and Organizational Studies 1023A/B Chapter Notes - Chapter 2: Free Cash Flow, Deferred Income, Issued Shares

7 Jun 2012

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

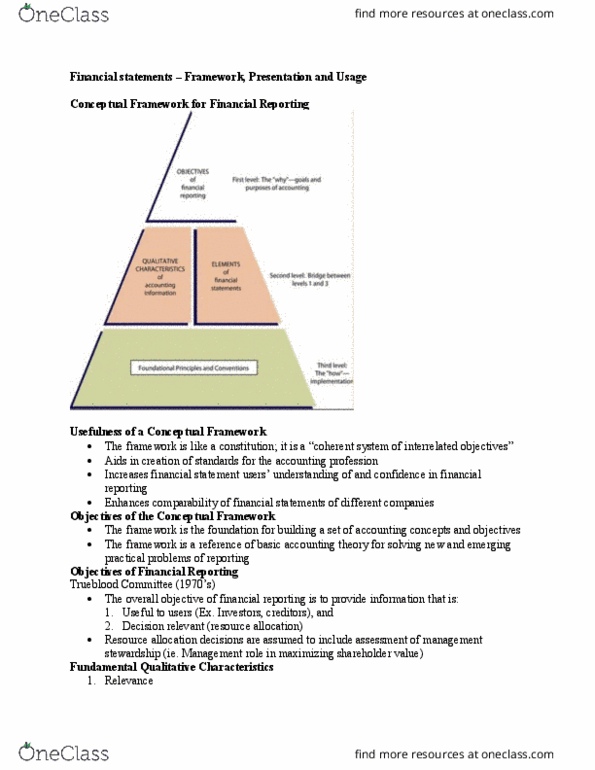

Guides : decisions about what to present in financial statements, alternative ways to document economic events and, appropriate ways of communicating this information. Why is it needed: ensures existing standards are clear and consistent, makes it possible to respond quickly to new issues, increases relevance, faithful representation, comparability and understandability of reports. Need: to develop a coherent set of standards and principles, to solve new and emerging practical problems. Main goal = provide information that is useful to individuals who are making the investment/credit decisions. Trueblood committee (1970s: all about forecasting for the future and determining future cashflows. Elements such as: amounts, timing and uncertainty of future cashflows, assets, liabilities and equity. How we can make informed decisions about financial statements: must have tradeoff along these characteristics. Cfa has relevance if it will make a difference in users" decisions. Predictive value helps users make predictions about the potential effects of past, present, future truncations or other events.