Management and Organizational Studies 1023A/B Chapter 5: MOS-Textbook-Notes-Chapter-5

8 Nov 2016

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

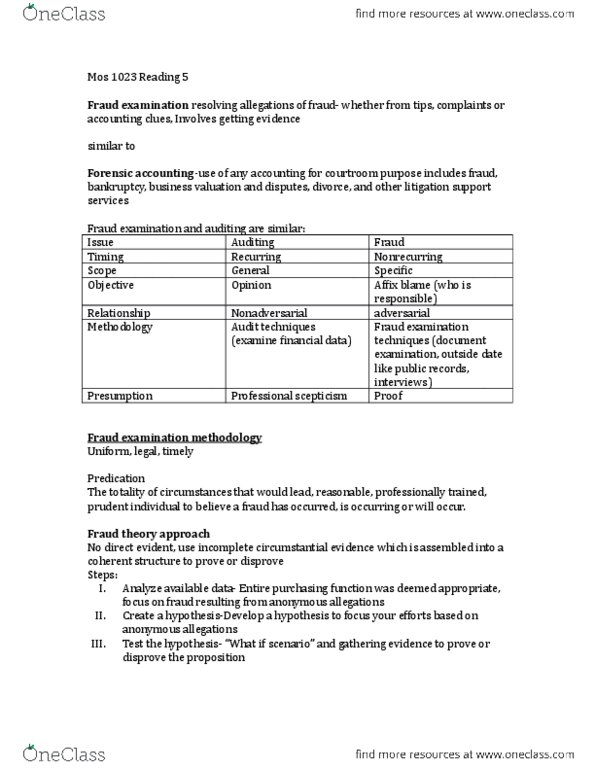

Fraud examination involves obtaining documentary evidence, interviewing witnesses and potential suspects, writing investigative reports, testifying to findings and assisting in the general detection and prevention of fraud. Forensic accounting the use of any accounting knowledge or skill for courtroom purposes. Non-recurring: conducted only regular basis with sufficient predication. Specific: conducted to resolve financial data specific allegations. Opinion: generally conducted to express an opinion on financial. Affix blame: determines whether fraud occurred and who is statements or related information responsible. Adversarial: involves efforts to to affix blame affix blame. Methodology audit techniques: primarily by examining financial data. Fraud examination techniques: conducted by - documentation examination, review of outside data (public records) and interviews. Proof: fraud examiners approach the resolution of a fraud by approach audits with attempting to establish sufficient professional skepticism proof to support or refute an allegation of fraud.