Management and Organizational Studies 1023A/B Chapter Notes - Chapter 5: Questioned Document Examination, Forensic Accounting, Affix

14 Dec 2015

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

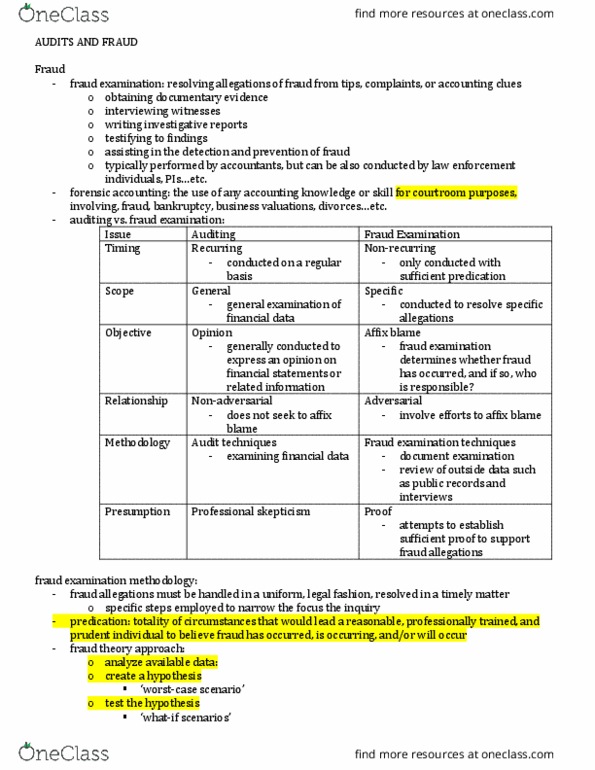

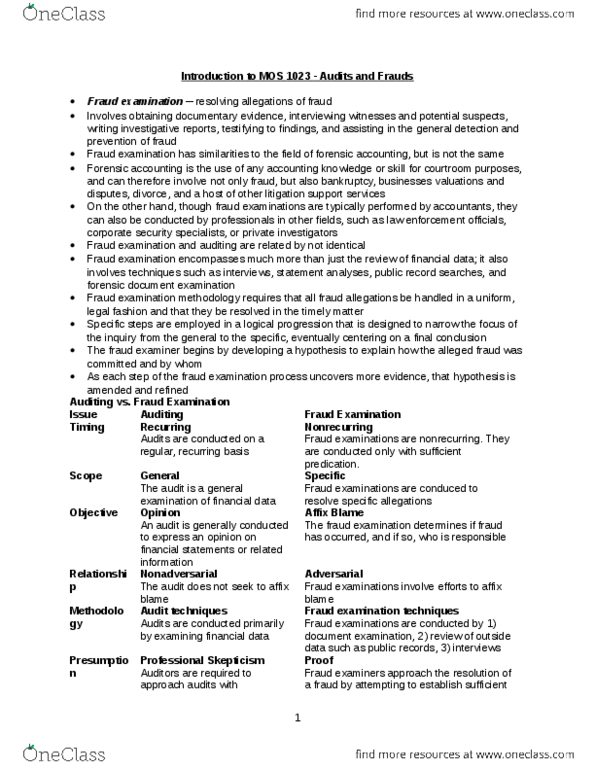

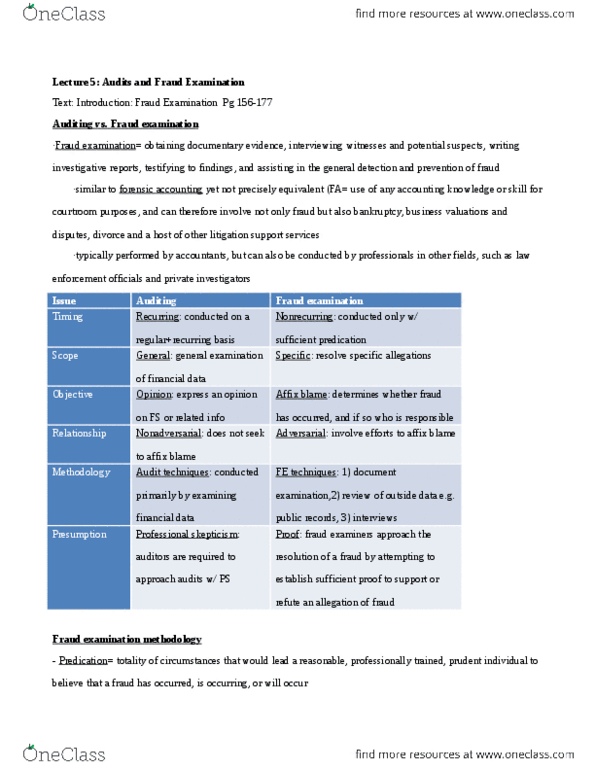

Fraud examination: the discipline of resolving allegations of fraud, from tips, complaint or accounting clues: typically performed by accountants, can also be conducted by professionals in other fields. Forensic accounting: use of any accounting knowledge or skill for. Fraud examination and auditing are related, but not identical. Because occupational frauds are financial crimes, certain degree. Fraud examination encompasses much more than just the review of auditing is necessarily involved of financial data; also involves techniques such as interviews, statement analyses, public records searches, and forensic document examination. Nonadversarial: audit process does not seek to affix blame. Audit techniques: conducted primarily by examining financial data. Professional scepticism: required to approach with professional scepticism. Specific: fraud examinations are conducted to resolve specific allegations. Affix blame: determines whether fraud has occurred and if so, who"s responsible. Fraud examination techniques: conducted by (1) document examination (2) review of outside data such as public records (3) interviews.