Management and Organizational Studies 3361A/B Chapter Notes - Chapter 15: John Wiley & Sons, Dividend, Retained Earnings

22 Mar 2013

School

Department

Professor

Document Summary

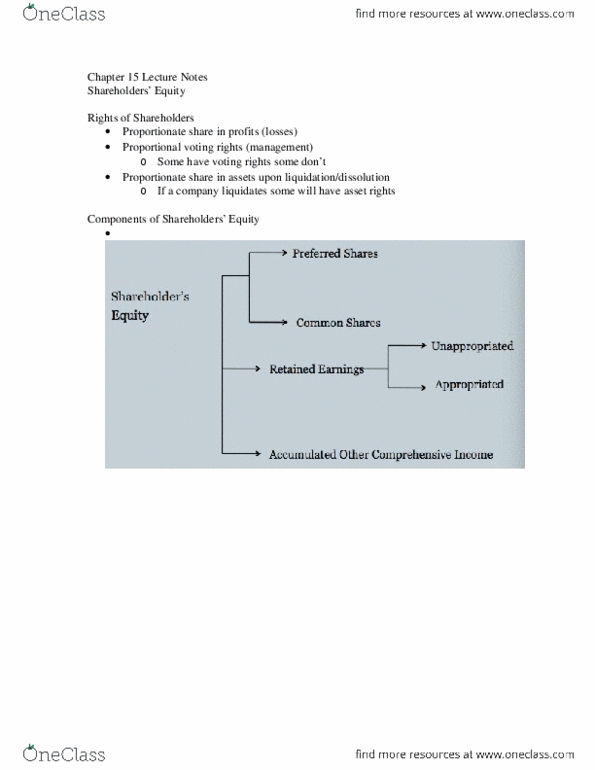

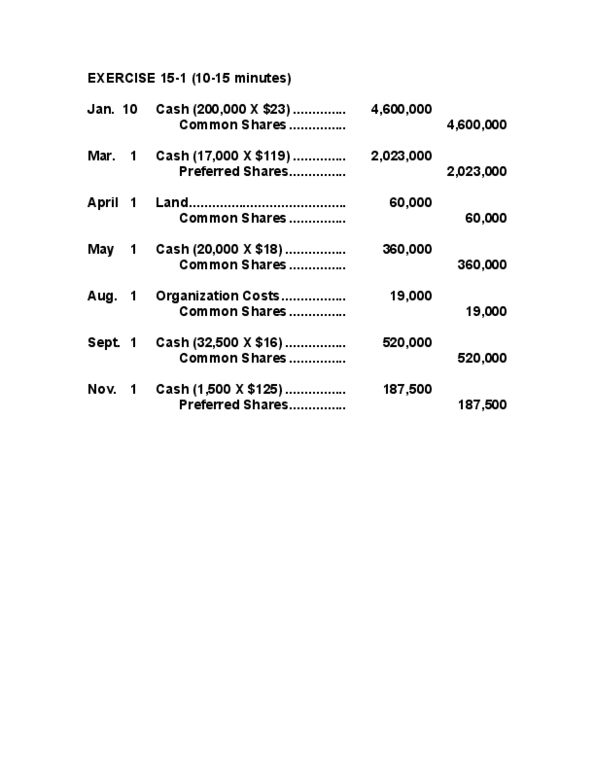

Exercise 15-3 (10-15 minutes) (a: cash [(6,000 x ) ,000] 178,000, land (3,750 x ) 120,000. Note: the market value of the share (,000) is used to value the exchange because it is a more objective measure than the appraised value of the land (,000). The original issue price of the individual shares being repurchased is not used. The original issue price of the individual shares repurchased would be considered in the total issue price for the class of shares but would be averaged with all other shares of the same class. ,000 ,000 ,000 (1) dividends in arrears: 25,000 x x 2 = ,000 (2) current year dividend: $ 180,000 per share participation threshold. (3) participating dividend: Since the common shareholders have received a per share dividend, per share is in excess of the dividend. Exercise 15-6 (continued) (b) retained earnings (c) common shares Cash (10,500 x ) (,800,000 / 60,000 x 10,500.