Management and Organizational Studies 3370A/B Chapter Notes - Chapter 6: Finished Good, Lean Manufacturing

14 Mar 2016

School

Department

Professor

Document Summary

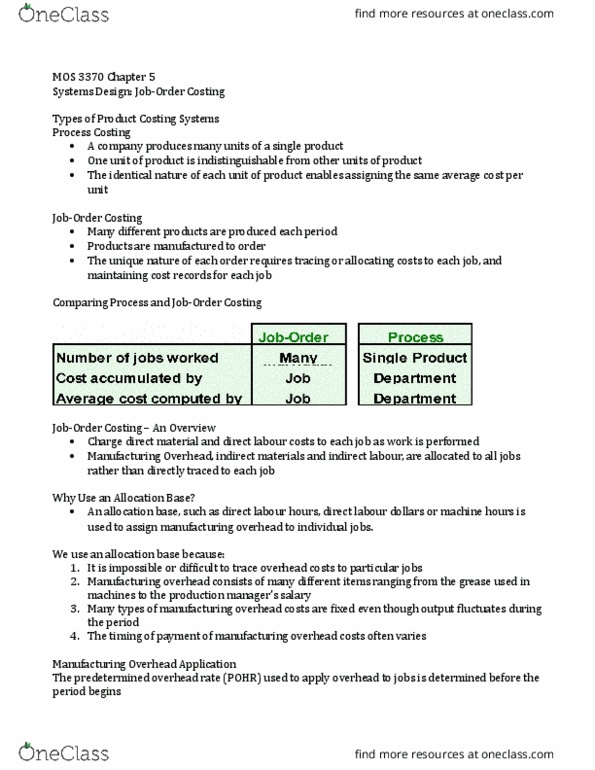

Both systems assign material, labour, and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use the same manufacturing accounts, including manufacturing overhead, Raw materials, work in process, and finished goods. The flow of costs through the manufacturing accounts is basically the same in both systems. Process costing is used when a single product is produced on a continuing basis or for a long period of time. Job-order costing is used when many different jobs having different production requirements are worked on each period. Process costing systems accumulate costs by department. Job-order costing systems accumulated costs by individual jobs. Process costing systems use department production reports to accumulate costs. Job-order costing systems use job cost sheets to accumulate costs. Process costing systems compute unit costs by department. Job-order costing systems compute unit costs by job on the job cost sheet. Process costing is used for products that are similar and produced continuously.