BU127 Chapter 12: BU127 Chapter 12 Notes.docx

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

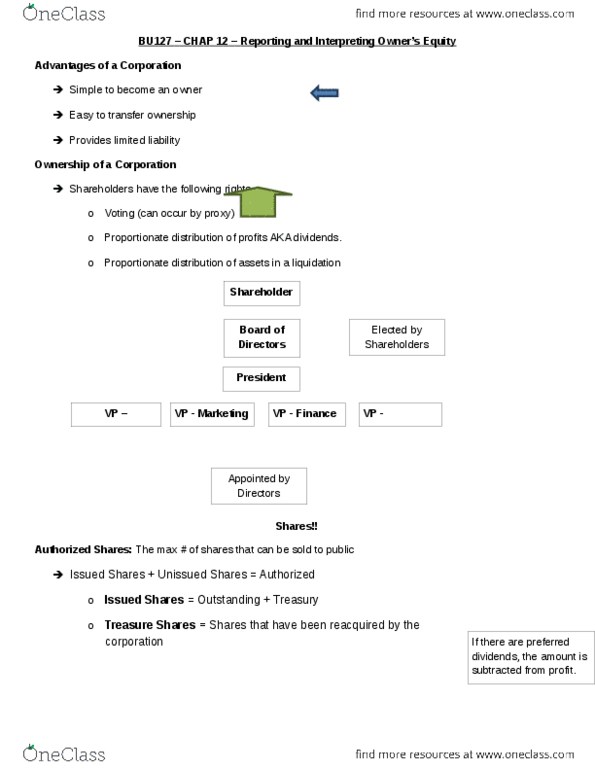

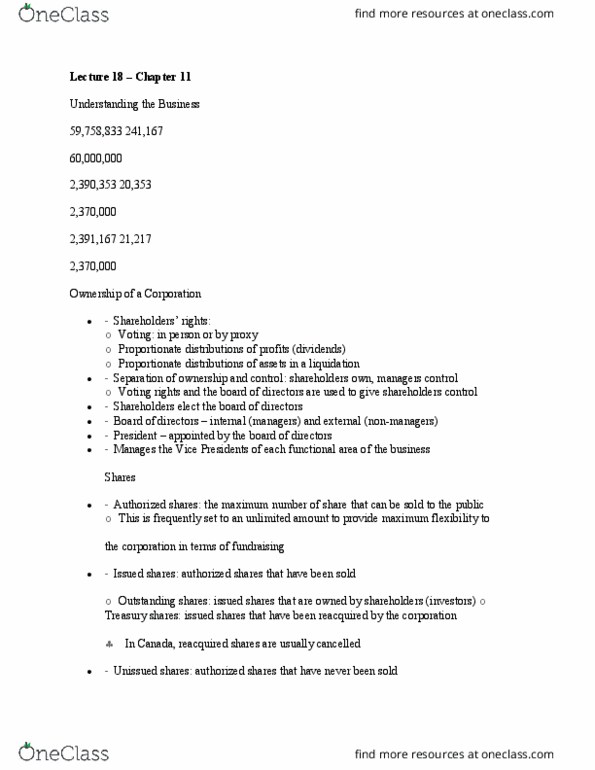

No par value and par value shares: par value: is the nominal value per share specified in the charter; it serves as the basis for legal capital, non par value shares: are shares that have no par value specified in the corporate charter, legal capital: is the permanent amount of capital, defined by law, that must remain invested in the business; it serves as a cushion for creditors. It can enter into contracts in its own name, be sued and is taxed as a separate entity: sole proprietorship: is an unincorporated business owned by one individual, partnership: is an unincorporated business owned by two or more people, good idea to draw up a contract between the partners, sole proprietorships or partnerships are neither legal entities and as a results owners may be directly sued and are individually taxed on the earnings of the business.