BU227 Chapter Notes - Chapter 11: Effective Interest Rate, Premium Bond, Interest Expense

Document Summary

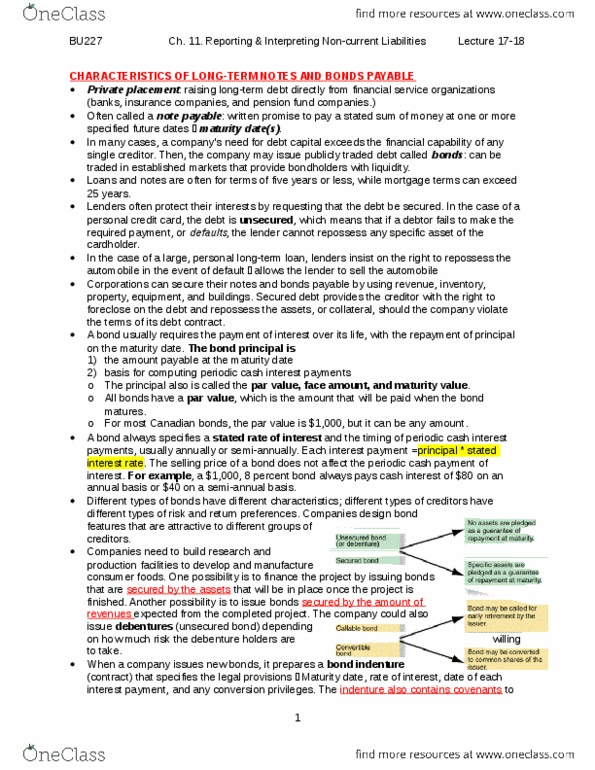

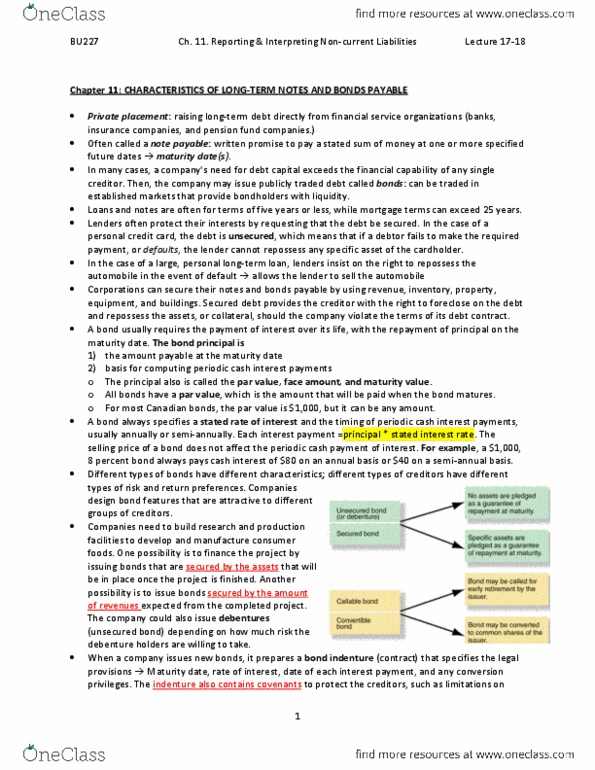

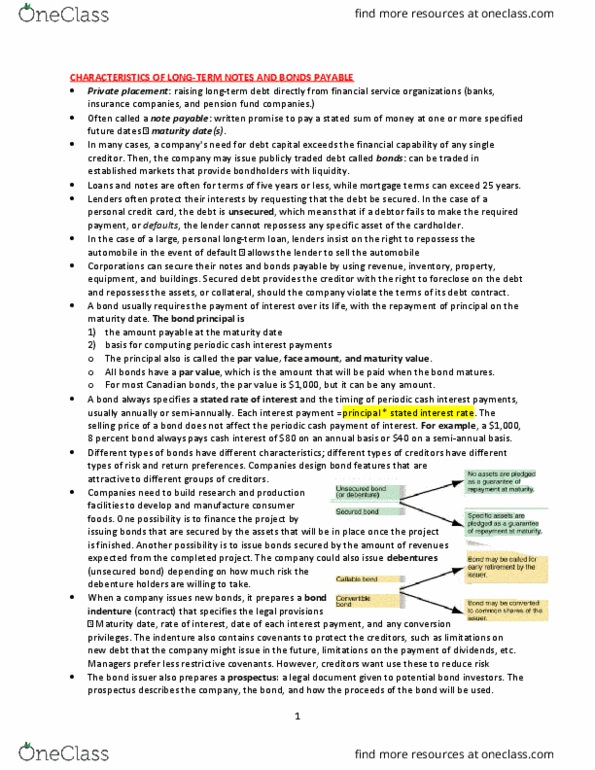

Companies can raise long-term debt directly from a number of financial service organizations, including banks, insurance companies, and pension fund companies raising debt from one of these organizations is known as private placement. In many cases, a company"s need for debt capital exceeds the financial capability of any single creditor. In these situations, the company may issue publicly traded debt called bonds. Lenders often protect their interests by requesting that the debt be secured rather than unsecured. In the case of a large, personal long-term loan such as an automobile loan, lenders will insist on the right to repossess the automobile in the event of default. A bond usually requires the payment of interest over its life, with the repayment of principal on the maturity date. Bond principal the amount payable at the maturity of the bond. It is also the basis for computing periodic cash interest payments.